The Sunday Drive - 04/28/2024 Edition [#108]

Musings and Meanderings of a Financial Provocateur

👋🏼 Hello friends,

Greetings from Saratoga Springs, NY. Let’s enjoy a leisurely Sunday Drive around the Internet.

🎶 Vibin'

Lots of corporate earnings were announced this past week, including some of the largest technology companies. For the week ended April 26th, the S&P 500 rose 2.7%1 and the Nasdaq 100 index was up 4%. Under the hood of a strong week in the equity markets however, the performance of the Magnificent 7 mega-tech stocks was all over the place, with AAPL up 2.1%, AMZN up 1.4%, GOOG up 10%, META down 8%, NVDA up 10.3%, MSFT up 1.3%, and TSLA up 18.5%.

We shall see what the coming week brings but for now, I’m vibin’ to Jump Around by the Irish rap band, House of Pain.

💭 Quote of the Week

“Knowing what you cannot do is more important than knowing what you can do.”

– Lucille Ball

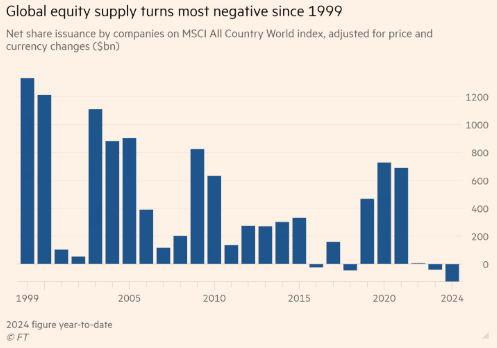

📈 Chart of the Week

The Chart of the Week highlights the recent global downturn in net equity share issuance.

Net equity share issuance refers to the difference between the number of shares issued by companies through initial public offerings (IPOs) and secondary offerings, and the number of shares repurchased or retired by those companies. This metric provides insight into the overall supply of publicly traded equity, which can have significant implications for stock market dynamics and investor behavior.

The current level of net share issuance is the most negative since 1999.

In the late 1990s, the net share issuance was positive, indicating that companies were issuing more new shares than they were repurchasing. This period was characterized by a surge in IPO activity and strong investor appetite for equities.

However, net share issuance turned negative in the early 2000s, coinciding with the bursting of the dot-com bubble and a period of increased share repurchases by companies. The net share issuance remained negative during the mid-2000s and early 2010s, reflecting the impact of the global financial crisis and the subsequent economic recovery.

The downturn in net equity share issuance is a global phenomenon, with varying degrees of impact across different regions. According to data from the MSCI All Country World Index, the Americas region exhibited the strongest performance in IPO activity compared to other regions, with 52 deals and $8.4 billion in proceeds in Q1 2024, up 21% and 178% year-over-year, respectively.2

In contrast, the Asia-Pacific region witnessed a significant decline in IPO activity, with 119 deals and $5.8 billion in proceeds in Q1 2024, down 34% and 56% year-over-year, respectively. This decline was particularly sharp in Mainland China and Hong Kong, with the number of deals decreasing by more than half and deal size falling by nearly two-thirds.3 The EMEIA (Europe, Middle East, India, and Africa) region experienced an impressive growth in IPO activity, launching 116 IPOs totaling $9.5 billion in Q1 2024, up 40% and 58% year-over-year, respectively. This surge was attributed to larger average deal sizes from IPOs in Europe and India.4

Why is this negative share issuance happening now, at a time of renewed strength in equity markets and continuing economic growth?

It's tough to say, but one could argue there are two major drivers:

Onerous regulations and the ready availability of private equity capital have made going public a lot less attractive in recent years.

Significant free cash flow generation by corporations of late, especially among the largest companies in the U.S., has made increased share repurchases the most efficient outlet for returning that cash to shareholders.

What might drive a renewal of growth in net equity share issuance? Several factors could contribute:

A slowdown in share repurchases could come either from valuation concerns or an economic slowdown. Also, the Inflation Reduction Act of 2022 imposed a 1% excise tax on share buybacks, which may discourage this practice.5

There are signs of a potential resurgence in IPO activity. The EMEIA region, especially India, has witnessed a surge in IPO activity, which could contribute to an increase in net share issuance.6

Equity-financed mergers and acquisitions have been a significant component of equity issuance in the past.7 A resurgence in M&A activity, driven by factors such as favorable economic conditions and access to capital, could lead to an increase in net share issuance.

The use of stock-based compensation has been a contributing factor to equity issuance, particularly in the technology sector.8 If companies increase the rate of share issuance via stock-based compensation, while at the same time conserving cash by slowing down share repurchase, we could see an increase in net share issuance.

Another conclusion one could draw from this week's Chart is a much simpler one. It's possible that investors competing with companies who are purchasing their shares creates a demand backdrop that more than offsets the diminishing supply of equity shares. In other words, simple supply and demand could greatly explain the recent equity market strength we’ve seen.

🚙 Interesting Drive-By's

🤔 A Harvard Medical School professor with ADHD shares how he retrained his brain - from Business Insider [Link]

📈 From Stagnation to Innovation: Japan's Economic Resurgence - from Jason Hsu [Link]

💡 Hype Deflation & Inflation - from Kyle Harrison [Link]

🤓 Capabilit Blindness and the Future of Creativity - from Dan Shipper [Link]

❤️ Moms welcome babies Johnny Cash and June Carter on same day, at same hospital - from Good Morning America [Link]

👋🏼 Parting Thought

Does this video reflect more poorly on the news media or the airlines? 🤷🏼♂️

If you have any cool articles or ideas that might be interesting for future Sunday Drive-by's, please send them along or tweet 'em (X ‘em?) at me.

Please note that the content in The Sunday Drive is intended for informational purposes only, and is in no way intended to be financial, legal, tax, marital, or even cooking advice. Consult your own professionals as needed. The views expressed in The Sunday Drive are mine alone, and are not necessarily the views of Investment Research Partners or Cache Financials.

I hope you have a relaxing weekend and a great week ahead. See you next Sunday...

Your faithful financial provocateur,

-Mike

If you enjoy the Sunday Drive, I'd be honored if you'd share it with others.

If this was forwarded to you, please subscribe and join the other geniuses who are reading this newsletter.

Source: YCharts for all return figures

Source: https://www.ey.com/en_gl/insights/ipo/trends

ibid. Note 2 above.

ibid. Note 2 above.

Source: https://budgetmodel.wharton.upenn.edu/issues/2023/3/9/the-excise-tax-on-stock-repurchases-effects

ibid. Note 2 above.

Source: https://www.morganstanley.com/im/publication/insights/articles/article_totalshareholderreturns.pdf

ibid. Note 7 above.