The Sunday Drive - 12/22/2024 Edition [#142]

Musings and Meanderings of a Financial Provocateur

👋🏼 Hello friends,

Greetings from snowy ❄️ Saratoga Spring, NY! 🐎

Christmas is just three days away and I’d like to wish you all a very Merry Christmas (or Happy Holidays if you prefer). 🎄

Now, let's take it easy and enjoy a leisurely Sunday Drive around the internet.

🎶 Vibin'

By this point in the Holiday season, we’re all getting a bit fatigued by all the Christmas music (which started around Halloween!)… So this week, I’m vibin’ to something a little different. Please enjoy Santa Claus is Back in Town by The Mavericks.

💭 Quote of the Week

“Never bet on the end of the world, because it only happens once.“

— Art Cashin (RIP)

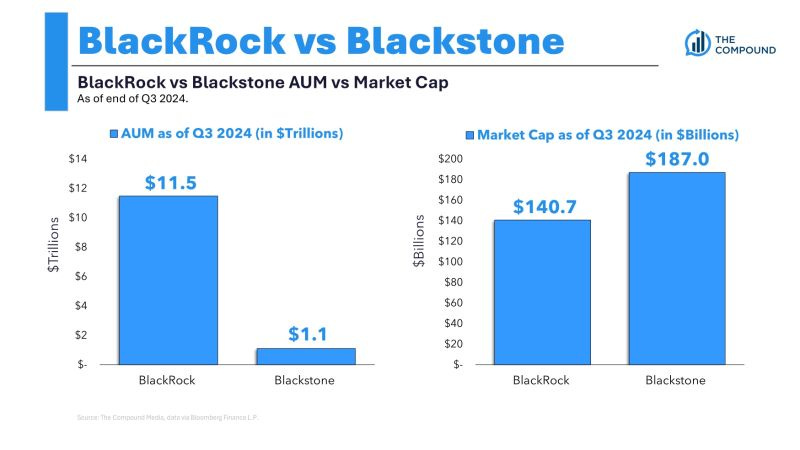

📈 Chart of the Week

It’s widely understood that the business model of private equity firms is more profitable than traditional asset managers, but the Chart of the Week really struck me.

At first glance, the numbers in the Chart seem quite puzzling. BlackRock manages an eye-popping $11.5 trillion in assets as of Q3 2024—ten times Blackstone's $1.1 trillion. Yet, Blackstone’s market cap ($187 billion) outstrips BlackRock’s ($140.7 billion). What’s going on here? Why does the market value private equity firms like Blackstone so much higher relative to their assets under management (AUM) compared to traditional asset managers like BlackRock?

Fee Structures: It’s All About Margins

BlackRock, as a traditional asset manager, generates much of its revenue through management fees tied to AUM. These fees are often razor-thin, especially in the passive investing space dominated by their flagship iShares ETFs. A typical fee for an index fund might be a fraction of a percentage point—say, 0.05%. It’s the ultimate high-volume, low-margin business.

Blackstone, on the other hand, operates in the high-margin world of private equity. The “2 and 20” model is legendary: 2% management fees and 20% performance fees (carried interest) on profits above a certain threshold. These performance fees can dwarf management fees, especially when private equity funds hit home runs with their investments. Higher margins mean higher profits per dollar of AUM, which the market rewards with a premium valuation.

Predictability vs. Upside

BlackRock’s revenue is highly predictable—it’s essentially a machine that hums along, clipping small fees off trillions of dollars in assets. While this predictability is valuable, it limits upside. Blackstone, however, thrives on less predictable (but often spectacular) outcomes. The market loves optionality, and Blackstone’s business model is built on it. If a private equity deal doubles or triples in value, those performance fees can skyrocket.

Asset Liquidity: A Double-Edged Sword

BlackRock’s AUM consists largely of liquid, publicly traded securities that investors can buy or sell any time they choose. This liquidity is great for clients but not necessarily for the firm’s valuation. Liquid assets mean money can flow out just as quickly as it flows in. Blackstone’s AUM, by contrast, is often locked up in illiquid investments like private companies, real estate, or infrastructure. Investors commit capital for years, giving Blackstone a more stable revenue stream and higher confidence in future cash flows.

Perception of Growth and Differentiation

Growth is another key factor. The passive investment industry, where BlackRock dominates, has seen fee compression due to intense competition. Blackstone operates in a space perceived as having more growth potential. Alternative investments, like private equity, real estate, and private credit, are increasingly in demand from institutional investors hunting for higher returns. This growth narrative adds to Blackstone’s premium.

Complexity and Risk Appetite

Finally, there’s an element of complexity—and the market’s appetite for it. Blackstone’s business is intricate, involving bespoke deals and creative financial engineering. The market values complexity (and the specialists who navigate it) in ways that don’t always apply to simpler, index-based investing.

Wrapping Up

The valuation discrepancy boils down to profitability, growth potential, and the market’s preference for the private equity business model. BlackRock may manage ten times more assets, but Blackstone’s ability to extract higher fees, lock in client capital, and chase outsized returns makes it the market’s favorite in terms of valuation.

Sources:

“BlackRock: A Financial Giant’s Dominance in Asset Management,” Investopedia.

“Private Equity Explained: Why 2 and 20 Still Reigns,” Harvard Business Review.

“The Rise of Alternative Investments,” McKinsey & Company.

🚙 Interesting Drive-By's

📈 How faster growth can offset America's debt problem. Really.

💡 Trump Tariffs Might Not Be So Bad

💰 The Case for Active Management in 2025

🤓 How AI Will Change Science Forever

🤔 Why Aging Experts Are Obsessed With ‘Health Span’

🎯 A New Age of Politics is Upon the World

👋🏼 Parting Thought

Let us not forget…

If you have any cool articles or ideas that might be interesting for future Sunday Drive-by's, please send them along or tweet 'em (X ‘em?) at me.

Please note that the content in The Sunday Drive is intended for informational purposes only, and is in no way intended to be financial, legal, tax, marital, or even cooking advice. Consult your own professionals as needed. The views expressed in The Sunday Drive are mine alone, and are not necessarily the views of Investment Research Partners or Cache Financials.

I hope you have a relaxing weekend and a great week ahead. See you next Sunday...

Your faithful financial provocateur,

-Mike

If you enjoy the Sunday Drive, I'd be honored if you'd share it with others.

If this was forwarded to you, please subscribe and join the other geniuses who are reading this newsletter.