The Sunday Drive - 12/07/2025 Edition [#192]

Musings and Meanderings of a Financial Provocateur

👋🏼 Hello friends! Let’s enjoy a leisurely Sunday Drive around the internet.

🎶 Vibin'

With the Holiday Season well underway, I can’t help but feel more connected than ever to my family, my friends, and my colleagues. I am truly blessed to have so many wonderful people in my life and I love them all.

So this week, I’m vibin’ to one of my favorite artists, I hope you enjoy Al Jarreau’s We’re In This Love Together.

💭 Quote of the Week

“Valuation is the closest thing to gravity in finance. Eventually, everything is pulled back towards intrinsic value.“

— Michael Mauboussin

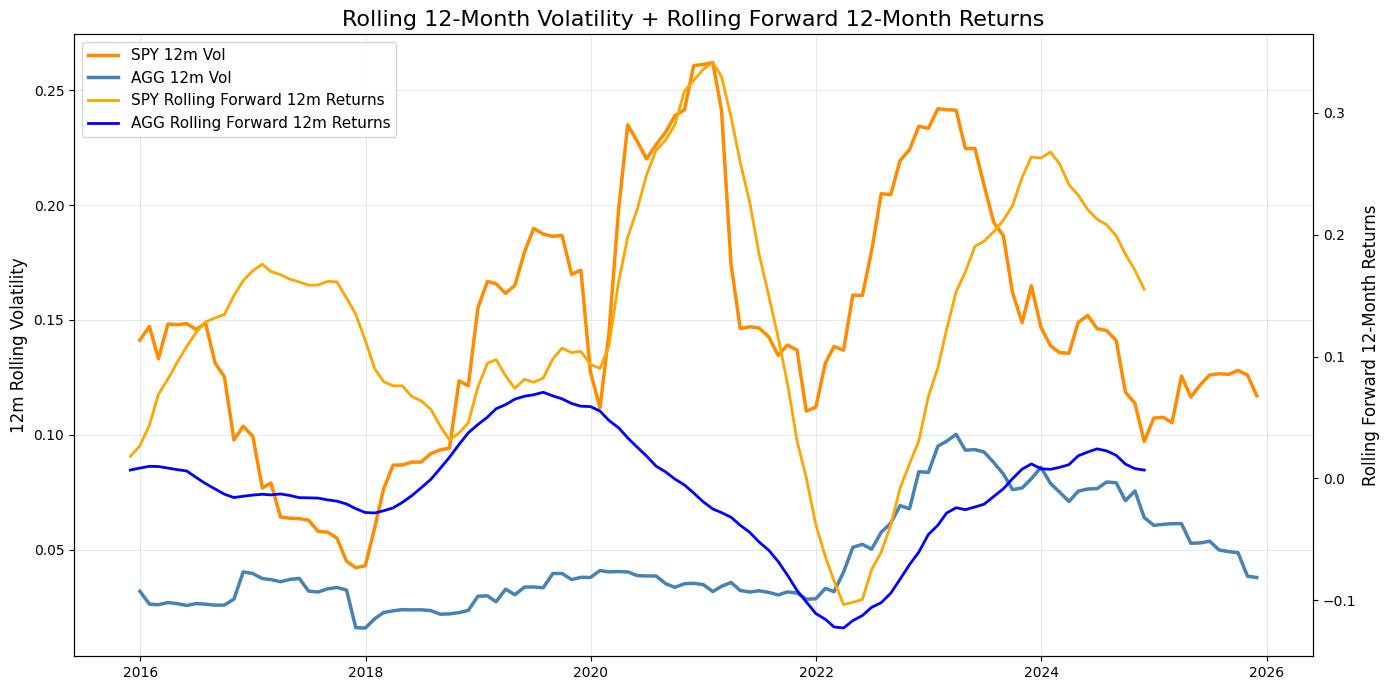

📈 Chart of the Week

A Few Thoughts on Volatility

The equity and bond markets have been eerily quiet of late, and it has gotten me thinking about volatility, or lack thereof, and what may lie ahead in 2026.

Every market environment carries a rhythm. Sometimes it’s steady and predictable; other times it’s chaotic and dissonant. But if you step back far enough, volatility has a way of revealing what’s happening beneath the surface, not by its level, which is what everyone seems to obsess over, but by its direction. That’s the insight that stood out to me in this week’s Chart, where I charted the rolling forward 12-month returns for both the SPDR S&P 500 ETF (SPY) and the iShares Core US Aggregate Bond ETF (AGG) alongside their rolling 12-month volatility, as represented by the standard deviation of returns.

Over the last decade, investors have lived through three distinct volatility regimes: the post-2015 normalization, the pandemic shock, and the AI-driven reflation period of 2022–2024. When you pair rolling 12-month volatility with rolling forward 12-month returns, a few patterns emerge which I think are worth unpacking, especially for those of us focused on risk-management and sequence-of-return dynamics.

Volatility Is a Laggard

First, volatility in equities has tended to behave like a coiled spring, and acts as more of a reaction function than a predictive one. Volatility spikes have historically coincided with stress events, as was the case in late 2018, early 2020, and 2022. In all three periods, forward returns troughed just ahead of the peak in volatility.

In other words, volatility tends to lag the deterioration or recovery in returns rather than lead it. Forward returns begin to weaken before the storm shows up in the volatility data. This isn’t surprising, but it’s an important reminder for anyone relying on backward-looking risk signals: by the time realized volatility warns you, the forward return story is already deteriorating.

Bonds Haven’t Recovered, Yet...

Second, the bond side of the chart (AGG) is equally revealing. The period from 2021–2023, and 2022 in particular, delivered the worst stretch for bonds in modern history.

But unlike equities, AGG’s forward return recovery has been slow, shallow, and incomplete. Even after volatility normalizes, the forward 12-month return profile remains muted. The relationship is tighter, more structural which tends to make bonds less responsive when volatility begins to fall. That’s a function of starting yields, duration risk, and the speed of the rate shock; bonds don’t generally bounce the way stocks do.

The Direction of Volatility Is What Really Matters

Third, the most useful conclusion for portfolio construction is that the direction of the volatility trend matters far more than the level. Rising volatility, regardless of whether it starts from 8% or 18%, generally aligns with weakening forward return prospects. Falling volatility, especially when it rolls over from an elevated level, has historically been a sign for improving forward equity performance.

For retirement-focused investors (and the advisors building plans for them), marrying volatility data with forward returns provides a framework that could be useful and help refine decisions around risk-budgeting, de-risking glidepaths, and the timing of protection overlays such as collars.

In short: volatility doesn’t predict returns, but the trend in volatility maps fairly well to the trajectory of returns. In my view, the real signal isn’t the magnitude of volatility—it’s the direction.

🚙 Interesting Drive-By's 🚙

🎯 Substance Over Form Shenanigans

🚀 Data Centers In Space Will Be the New Normal In a Decade

💯 Teaching Students To Think, Not Just Scroll, In the Age of AI

🤔 Amazon Release AI Agents That Can Work For Days At a Time [$WSJ]

💡 The Rise of the Traveling Third Space

👋🏼 Parting Thought

If you have any cool articles or ideas that might be interesting for future Sunday Drive-by's, please send them along or tweet 'em (X ‘em?) at me.

Please note that the content in The Sunday Drive is intended for informational purposes only, and is in no way intended to be financial, legal, tax, marital, or even cooking advice. Consult your own professionals as needed. The views expressed in The Sunday Drive are mine alone, and are not necessarily the views of Investment Research Partners.

I hope you have a relaxing weekend and a great week ahead. See you next Sunday...

Your faithful financial provocateur,

-Mike

If you enjoy the Sunday Drive, I'd be honored if you'd share it with others.

If this was forwarded to you, please subscribe and join the other geniuses who are reading this newsletter.

Thesaurus!