The Sunday Drive - 10/12/2025 Edition [#184]

Musings and Meanderings of a Financial Provocateur

👋🏼 Hello friends! Let’s enjoy another leisurely Sunday Drive around the internet.

🎶 Vibin'

In keeping with this week’s theme of the impact of diminished purchasing power in the post-COVID economy, I’m vibin’ to Jeff Beck (RIP) and Billy Gibbons (of ZZ Top fame) performing Tennessee Ernie Ford’s classic Sixteen Tons.

💭 Quote of the Week

“’Steve Jobs famously imagined the computer as a bicycle for the mind. If the computer is a bicycle, perhaps AI is an e-bike.“

— Josh Brake

📈 Chart of the Week

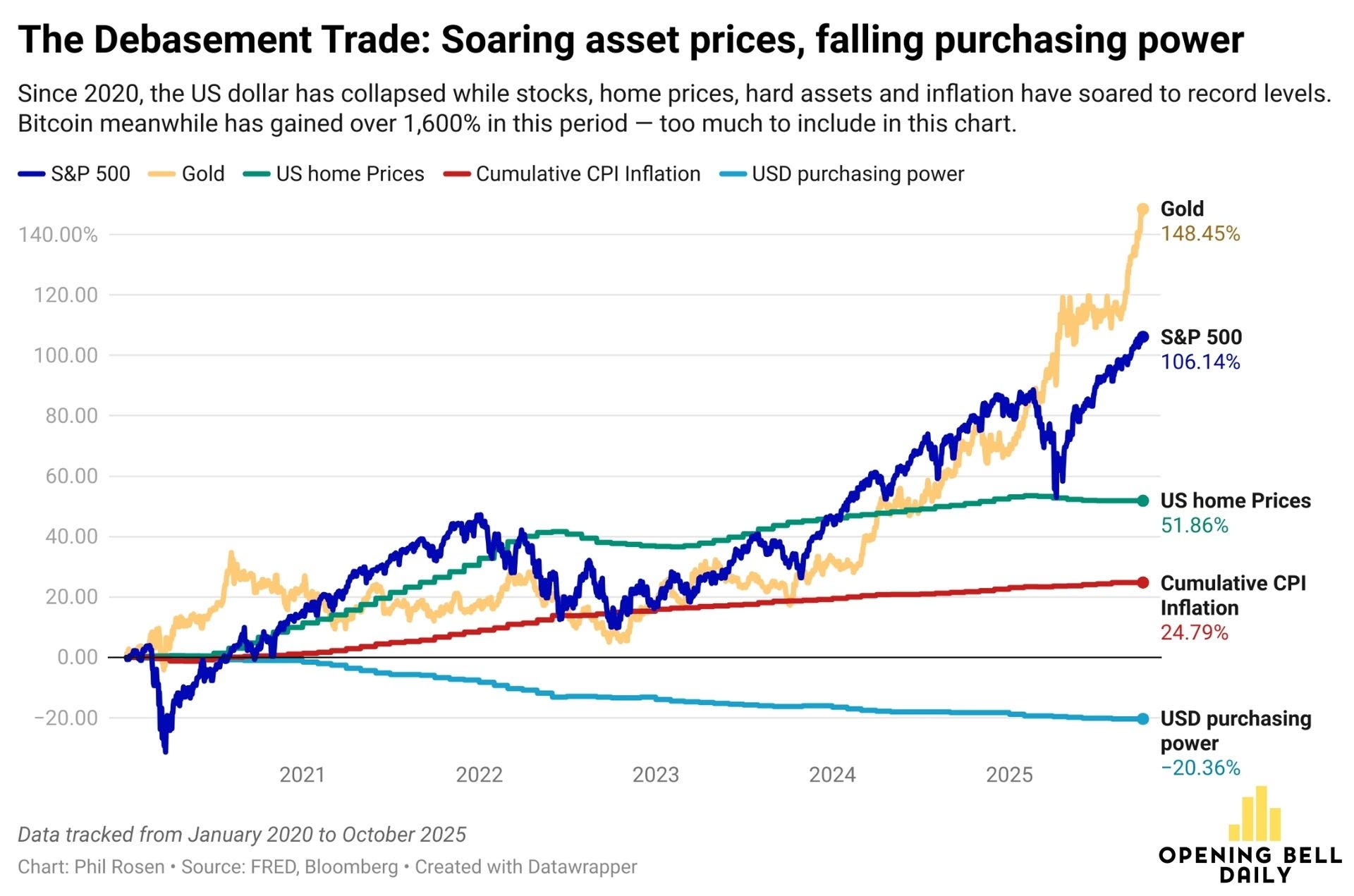

The Chart of the Week captures one of the defining investment narratives of the post-2020 era: the so-called “Debasement Trade.” In simple terms, the purchasing power of the U.S. dollar has steadily eroded while asset prices—stocks, homes, gold, and inflation-linked measures—have soared.

Since January 2020, gold has risen roughly 148%, the S&P 500 is up over 106%, and U.S. home prices have climbed nearly 52%. Over that same period, the purchasing power of the U.S. dollar has fallen more than 20%. Cumulative CPI inflation has risen just under 25%, but that understates the impact of debasement on real wealth. Asset inflation has far outpaced consumer price inflation.

For consumers, this dynamic is a slow squeeze. Wages typically lag both inflation and asset appreciation, meaning that the cost of buying a home, funding education, or saving for retirement rises faster than incomes. Dollar weakness magnifies this effect over time. It’s a difficult conundrum with no easy answers.

For investors, debasement has turbocharged nominal asset returns, especially in scarce or hard assets—equities, real estate, gold, and even Bitcoin. As long as this dynamic remains in place, it adds to the importance of owning assets that maintain or grow real purchasing power over time.

For policymakers, persistent dollar weakness complicates everything: it supports asset markets and export competitiveness but risks un-anchoring inflation expectations. In that environment, monetary and fiscal policy makers walk an increasingly difficult tight rope—too much stimulus accelerates debasement, too much restraint risks growth shocks.

How much longer the “Debasement Trade” continues will depend heavily on fiscal discipline, monetary policy, and global confidence in the dollar as a reserve currency.

To me, it seems to be a very crowded trade, but it could continue for quite a while.

I believe that investors who sniff out signs of a turn in the dollar and position their portfolios accordingly could be well rewarded. But, it’ll certainly take patience.

Sources: St. Louis Federal Reserve, Bloomberg, U.S. Bureau of Labor Statistics

🚙 Interesting Drive-By's 🚙

💡 The New Cognitive Aristocracy: This is Not the End of Thinking

📉 Japanification—Coming to America by 2031?

📈 Why AI Job Loss is Actually Job Liberation

🎯 The Tariff Exemption Behind the AI Boom

👋🏼 Parting Thought

This past Friday…

If you have any cool articles or ideas that might be interesting for future Sunday Drive-by's, please send them along or tweet 'em (X ‘em?) at me.

Please note that the content in The Sunday Drive is intended for informational purposes only, and is in no way intended to be financial, legal, tax, marital, or even cooking advice. Consult your own professionals as needed. The views expressed in The Sunday Drive are mine alone, and are not necessarily the views of Investment Research Partners.

I hope you have a relaxing weekend and a great week ahead. See you next Sunday...

Your faithful financial provocateur,

-Mike

If you enjoy the Sunday Drive, I'd be honored if you'd share it with others.

If this was forwarded to you, please subscribe and join the other geniuses who are reading this newsletter.