The Sunday Drive - 07/12/2026 Edition [#223]

Musings and Meanderings of a Financial Provocateur

👋🏼 Hello friends! Let’s enjoy another Sunday Drive around the Internet.

🎶 Vibin’

This week saw an increase in geo-political tensions in both Iran and Russia. Commodities were up, but not a lot. Bonds were down, but not a lot. The S&P 500 was up, but not a lot. Other equity markets were down, but not a lot. So all in all, the markets pretty much just said, “I don’t care…. on to Q2 earnings season.”

So this week, I’m vibin’ to I Love It! from the Swedish Pop Duo, Icona Pop. 🤷🏼♂️

💭 Quote of the Week

“Management is doing things right; leadership is doing the right things.”

— Peter Drucker

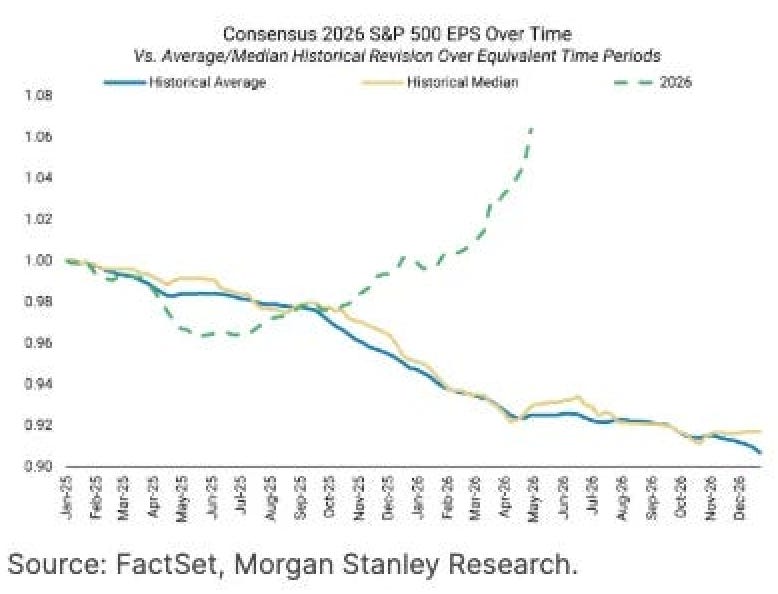

📈 Chart of the Week

📈 The Estimates Are Climbing, And That’s The Weird Part

The most dangerous words in investing are “this time is different.” This week’s Chart does show us something that looks different. You can decide if it is.

Sell-side analysts almost always start the year too optimistic, then walk their numbers down as reality sets in. Over the past 20 years, the bottom-up EPS estimate for a given quarter has fallen an average of 4.2% while that quarter was still in progress. Down over five years (2.0%). Down over ten (2.7%). Down basically always.

2026 seems to have broken the pattern. Analysts raised the Q2 estimate by 3.4% during the quarter, the largest in-quarter increase since 2021. The full-year 2026 number climbed 6.3% in just three months, from about $320 to $340 per share. That green line in the Chart is heading up while every historical version heads down.

So what’s driving it? Two things, mostly. Energy estimates for the year jumped 41% on firmer prices. And the AI infrastructure trade kept feeding on itself, with Information Technology and Communication Services full-year estimates up 9% and 12%, respectively. Companies are guiding higher too. Of the S&P 500 names that gave Q2 guidance, 57% guided up, against a 41% norm. And revenue backs up the profit story: Q2 sales are tracking 12.2% growth, the best in three years. So there’s a real business underneath the optimism.

But here’s where I get nervous. This growth is narrow. Nine of eleven sectors saw their 2026 estimates rise, but the dollars are quite lopsided. Three companies, Alphabet, Amazon, and Meta, account for roughly 70% of the entire increase in 2026 earnings expectations. Strip out a handful of names and the picture goes back to ordinary.

The full-year number is genuinely big: 24% expected growth, against just under 10% in 2024 and about 12% in 2025. Call it what it is. A small group of enormous companies hoping (promising?) to earn their way into some very large capital expenditure budgets. Those same three have guided to combined 2026 capex of roughly half a trillion dollars. The estimates assume that spend turns into profit, on schedule.

Maybe it does. A lot is going right, and I’m not betting against these franchises. But concentrated growth is concentrated risk, dressed up as an index. When three stocks carry the number, three disappointments carry it back down. The estimates went up for once. They can still come down the ordinary way.

Sources: FactSet Earnings Season Preview: Q2 2026 · FactSet: Largest Increases to Quarterly EPS Estimates Since 2021 · 24/7 Wall St: Just 3 Companies Drive 70% of the S&P 500’s 2026 Growth Expectation

🚙 Interesting Drive-By’s 🚙

💸 Hyperscaler Capex to Exceed Cash Flow by Q3 2026 - Epoch AI’s Isabel Juniewicz pulls straight from SEC filings to show operating cash flow at the five biggest hyperscalers growing about 23% a year while capex grows about 70%, with the lines crossing to zero free cash flow around Q3 2026. Oracle has already crossed and Amazon is crossing now, so the AI buildout is about to be funded with debt and fresh equity rather than cash on hand, the moment the risk stops being hypothetical.

🤔 The Real Economy Comeback No One Saw Coming - Anthony Pompliano leans on Jim Bianco’s data showing that in one down week the S&P fell about 2% while the roughly 425 non-AI names rose 2.3%, a rare crack in the everything-is-AI trade. He reads it as capital rotating from buybacks back to real capex, though a single week of breadth is a thin reed to hang a regime change on.

🤓 Stretch Marks: A Case Study in Financial Engineering - Marc Rubinstein dissects Strategy’s funding machine, now holding 847,363 bitcoin, roughly 4% of all that will ever exist, propped up by a preferred-stock structure that has raised over $10 billion since last summer. With bitcoin down about 30% this year, it’s a clean study of how fast financial engineering turns from clever to fragile once the underlying asset stops cooperating.

💡 Invisible Companies - Jay Barney, Haiyang Zhang, and Jerry Neumann argue the most durable edge isn’t a moat but “competitive neglect,” the boring, low-status businesses nobody bothers to notice, the way Constellation Software compounded at roughly 34% a year since its 2006 IPO against Berkshire’s 11% by buying niche software everyone else ignored. The risk they flag at the close: if every AI is trained on the same datasets and playbooks, invisibility either gets stripped away or quietly hardcoded, and spotting what the models can’t see may become the last advantage left.

🤔 On the Inevitability of an AI Bubble - Ben Carlson revisits his own 2023 call that an AI bubble was inevitable, noting Nvidia has gone from a $755 billion company then to north of $5 trillion now, with tech and communication services together half the S&P 500. He argues it may still not qualify as a bubble under Asness’s definition, which is either reassuring or exactly what you’d expect to hear near a top.

🤔 29 Loaded - Jack Raines marks turning 29 with a list of reflections that double as risk lessons, from “optionality is a depreciating asset” to “perceived risk is usually an exaggeration of realized risk.” The one worth taping to a screen: the utility of money depreciates with age, so hoarding it for a someday that keeps receding carries its own quiet cost.

👋🏼 Parting Thought

Manic markets be like…

If you have any cool articles or ideas that might be interesting for future Sunday Drive-by’s, please send them along or tweet ‘em (X ‘em?) at me.

Please note that the content in The Sunday Drive is intended for informational purposes only, and is in no way intended to be financial, legal, tax, marital, or even cooking advice. Consult your own professionals as needed. The views expressed in The Sunday Drive are mine alone, and are not necessarily the views of Investment Research Partners.

I hope you have a relaxing weekend and a great week ahead. See you next Sunday...

Your faithful financial provocateur,

-Mike

If you enjoy the Sunday Drive, I’d be honored if you’d share it with others.

If this was forwarded to you, please subscribe and join the other geniuses who are reading this newsletter.