The Sunday Drive - 07/05/2026 Edition [#222]

Musings and Meanderings of a Financial Provocateur

👋🏼 Hello friends! This weekend, I’d like to wish a Happy 250th Birthday to the greatest nation on earth. 🇺🇸

Celebrate with me as we enjoy another Sunday Drive around the Internet.

🎶 Vibin’

This is the 222nd edition of the Sunday Drive and it marks a return once again of the only Vibe of the Week that we’ve ever repeated. As in prior years, I’m again vibin’ to the legendary Whitney Houston (RIP) and her performance of the Star Spangled Banner at the 1991 Super Bowl.

It is the most beautiful rendition of our National Anthem that I’ve ever heard, and is an annual tradition for the July 4th edition of The Sunday Drive. 🇺🇸

💭 Quote of the Week

“The preservation of the sacred fire of liberty, and the destiny of the republican model of government, are justly considered as deeply, perhaps as finally, staked on the experiment entrusted to the hands of the American people.”

— George Washington, First Inaugural Address, April 30, 1789

📈 Charts of the Week

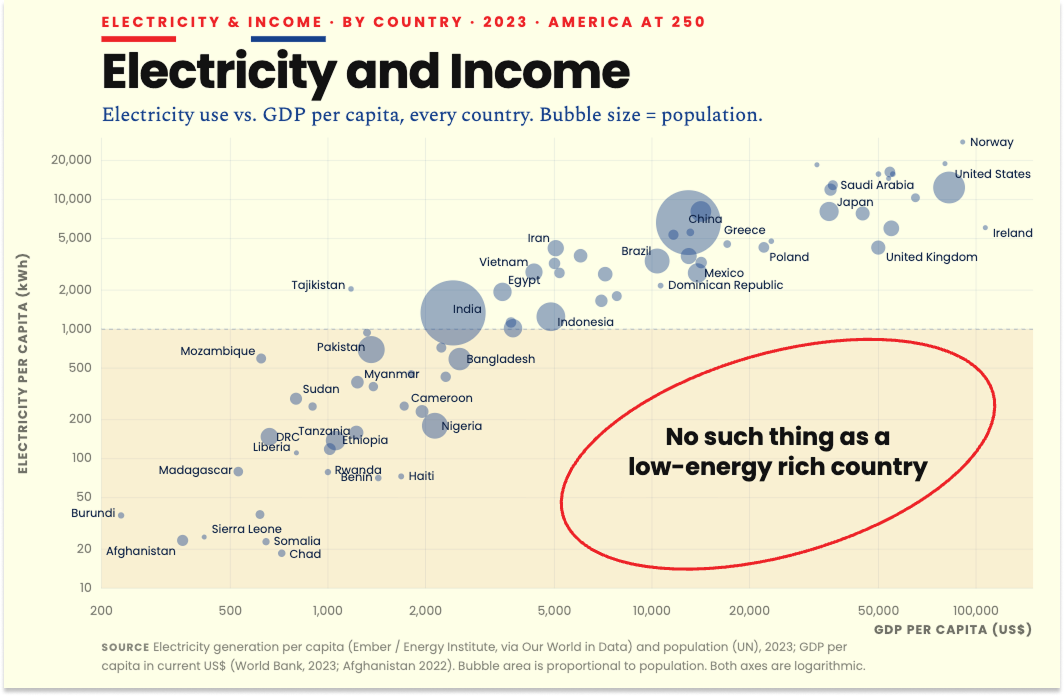

⚡ No Country Gets Rich In the Dark, But There’s a Price

The first Chart this week reminds us that there’s no such thing as a low-energy rich country. Every economy in the top-right corner uses a lot of electricity per person. Every one down in the bottom-left does not. Wealth and watts travel together, and they have for a century.

For the last 40 years or so, domestic GDP kept climbing while electricity demand stayed flat. We got more efficient, shipped heavy industry overseas, and swapped incandescent bulbs for LEDs. Growth without more power. That era just ended.

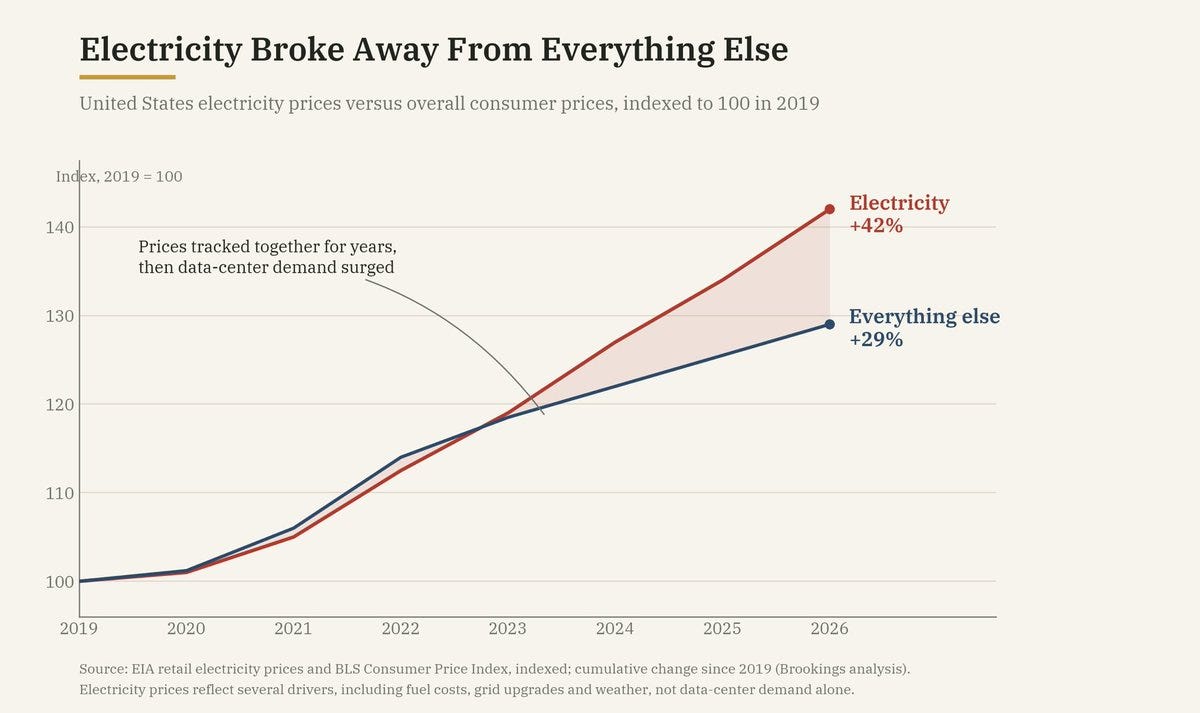

This week’s second Chart shows that since 2019, US electricity prices are up 42% while everything else in the goods and services basket rose 29%. The two lines tracked each other for years, then split around 2023, right as data-center demand started to kick in. I should point out that fuel costs, grid upgrades, and weather feed that number too, so this isn’t AI alone. But the timing is hard to ignore.

Data centers used roughly 4.4% of US electricity in 2023. Berkeley Lab’s range for 2028 runs from 6.7% to 12%. Even the low end is a demand shock the grid hasn’t felt since air conditioning went mainstream.

So does more electricity mean more GDP? Perhaps, maybe even probably. The first Chart shows a correlation, and a correlation won’t tell you which way the arrow points. Rich countries use lots of power because they do lots of valuable things, not the reverse. If the new watts run AI that genuinely lifts productivity, we’ll see accelerating real growth. If they run models that never earn their keep, you could end up with a very expensive space heater and a write-down.

Now let’s consider the supply side, which is where this gets interesting.

Start with the more traditional way of adding power: burn gas. New turbines carry 5-to-7-year wait times. GE Vernova is booked into 2029. Grid interconnection queues run 5 to 6 years, and the average project waits more than 2,100 days just to plug in. Demand gets signed in quarters. Firm gas-fired capacity shows up in years.

Gas isn’t the only source of new electricity supply. In 2025, solar and battery storage were about 81% of all new US generating capacity, and the EIA expects solar, wind, and batteries to be more than 99% of what gets added in 2026. Solar alone is more than half of it. A solar farm goes from permit to power in months, not the better part of a decade. So the fastest new electricity supply in America is already renewable, by a wide margin.

The catch: the sun doesn’t shine at night, and a data center wants a steady gigawatt around the clock. Solar paired with batteries firms a lot of that load, though not all of it, and the same interconnection queue that slows gas slows renewables too. So cheap solar bends the cost curve down without fully solving the “always-on power right next to the campus” problem.

Then there’s the wild card, which is highly speculative and one we’ve talked about before: move the data center off the planet.

Orbital compute stopped being pure science fiction in the past year. SpaceX is the acknowledged frontrunner, but there are others as well. Google’s Project Suncatcher plans to put its own AI chips in orbit, with prototype satellites targeted for early 2027. Starcloud launched a satellite carrying an Nvidia H100 in late 2025 and is already talking about a 5-gigawatt, solar-powered cluster in space. Axiom Space put its first data-center nodes in low earth orbit this past January. The pitch is simple physics: in the right orbit a solar panel is up to 8 times more productive than on the ground and generates almost continuously, with no land to fight over and no local ratepayer footing the bill.

But let’s not get carried away just yet. Some speculate that launch costs need to fall by roughly an order of magnitude for the economics to work, and radiation and on-orbit servicing are still unsolved at scale. This likely relieves nothing on the grid this decade. But directionally it’s the pressure valve. If even a slice of AI training eventually runs on free sunlight in orbit instead of a gas plant in Ohio, some of the demand pushing up terrestrial electricity prices lifts off with it.

Which brings us back to the price question. Will more supply cool the increases? Not soon. The demand looks price-inelastic where it counts, because a hyperscaler spending tens of billions on chips doesn’t really flinch at its power bill. Cheap solar shaves the cost of each new megawatt, and orbital compute might someday route demand off the grid entirely, but near term the marginal buyer sets the price and it climbs until something breaks.

The spread between those two lines in the second Chart two is very much something we should keep an eye on. I believe it will have significant bearing on economic growth here in the U.S. as well as on the upcoming mid-term elections, and even more so on the 2028 election.

Sources: Berkeley Lab, 2024 United States Data Center Energy Usage Report · EIA via Electrek: 99%+ of new US capacity in 2026 will be solar, wind + storage · S&P Global: US gas-fired turbine wait times as much as seven years · Utility Dive: GE Vernova gas turbine backlog into 2029 · DCD: Google Project Suncatcher · GeekWire: Starcloud space-based data centers

🚙 Interesting Drive-By’s 🚙

🇺🇸 From Promise to Turning Point: The Road to the Battles of Saratoga - Sean Kelleher (Past’s Paths) walks the 1777 northern campaign that turned Burgoyne’s tidy Hudson-corridor plan into the collapse that brought France in and made the Revolution global, a hometown turning-point story timed to Saratoga 250 and the July 4th festivities at the Race Course.

🤔 The Cost of Status - Jack Raines (Young Money) makes the case that the kid with $700,000 sunk into his schooling by 18 has the most to lose, since the prize for winning a finite status game is only entry into the next one, a sharp counterweight to the wealth-transfer optimism running through retirement planning right now.

🧠 On the Production and Dissemination of Knowledge in the AI Era - Cyril Hédoin (The Archimedean Point) argues AI companies are running the academic-publishing playbook, training for free on knowledge they never paid for and then fencing it behind subscriptions that jump from $25 to $200 a month, with the real hold-up arriving once businesses are too dependent to walk away.

🤓 10-Year Treasury Yield Long-Term Perspective: June 2026 - Jennifer Nash (Advisor Perspectives) stacks six decades of the 10-year against the Fed funds rate and inflation, and June’s read is the tell: a 4.44% yield against 4.25% inflation leaves a real yield near zero, with FedWatch pricing a 27% chance of a hike rather than a cut, the sticky-inflation setup where equities keep trusting the bond market to do the Fed’s fighting.

🤔 The Occupational Hazard of Wisdom - Chip Conley (Wisdom Well) lands a jolt of a stat: of the five figures people name as history’s wisest, four (Gandhi, Jesus, MLK, Socrates) were murdered and the fifth, Confucius, was never hired, his point being that real wisdom takes the courage to stand apart, not another credential to accumulate.

⚽ Why ‘High-Emotional’ Videos of World Cup Tourists Are Going Viral - Northeastern researchers note the same algorithms that usually reward doomscrolling are now boosting feel-good clips of Scots in traffic cones and Europeans discovering ranch dressing, a rare burst of celebratory globalism landing right as Pew has U.S. favorability near its lowest since 2002, proof there’s still a market for human connection in an algorithm-driven world.

👋🏼 Parting Thought

Getting your point across…

If you have any cool articles or ideas that might be interesting for future Sunday Drive-by’s, please send them along or tweet ‘em (X ‘em?) at me.

Please note that the content in The Sunday Drive is intended for informational purposes only, and is in no way intended to be financial, legal, tax, marital, or even cooking advice. Consult your own professionals as needed. The views expressed in The Sunday Drive are mine alone, and are not necessarily the views of Investment Research Partners.

I hope you have a relaxing weekend and a great week ahead. See you next Sunday...

Your faithful financial provocateur,

-Mike

If you enjoy the Sunday Drive, I’d be honored if you’d share it with others.

If this was forwarded to you, please subscribe and join the other geniuses who are reading this newsletter.