The Sunday Drive - 06/28/2026 Edition [#221]

Musings and Meanderings of a Financial Provocateur

👋🏼 Hello friends! Let’s enjoy another Sunday Drive around the Internet.

🎶 Vibin’

I expect tonight to be an exciting and cathartic evening. My son and I will have the good fortune to see Rush in concert tonight at Dickie’s Arena in Ft. Worth, TX, my hometown. Rush was my favorite band in high school and beyond, and I’m thrilled beyond belief that I get to see them once again after the loss of their beloved drummer, The Professor, Neil Peart (RIP). Anika Niles, the drummer they’ve found to join them on their 50-Something Tour is truly a phenom and apparently doing a great job stepping into perhaps the biggest shoes in rock-n-roll history. I can’t wait to see that for myself.

An added bonus this weekend has been the opportunity to spend time with my brother and his family, as well as getting my Tex-Mex and BBQ fix on top of that!

So many songs to choose from… but I am vibin’ this week to Limelight because it’s going to be great to see them in it once again. Enjoy.

💭 Quote of the Week

“Don’t try to buy at the bottom and sell at the top. It can’t be done except by liars.”

— Bernard Baruch

📈 Chart of the Week

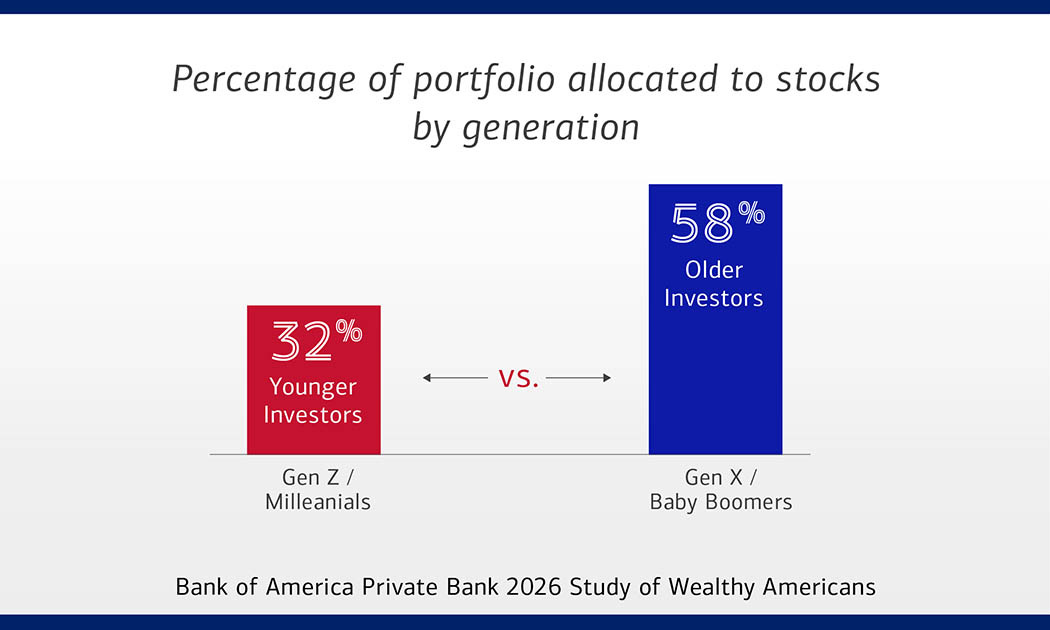

👴🏼 The Kids Are De-Risking the Wrong Direction

This week’s Chart is from a Bank of America study of households with $3M+ in assets which found Gen Z and Millennial investors holding just 32% of their portfolios in stocks, as compared to 58% for the Gen X and Boomer crowd. The gap gets filled with 15% in alternatives and 13% in crypto. Two-thirds of the youngsters told BofA they no longer believe stocks and bonds can deliver above-average returns. Not an earth shattering finding but interesting nonetheless.

Certainly older investors have built significant wealth over the last 40 years, in large part from equity markets, The younger investing cohort hasn’t had time to do that yet.

But...

An interesting question is what longevity does to the math underneath all of this.

Ninety-two percent of these same wealthy households told BofA that longer life expectancy is now a core factor in their planning. Fair enough. We’ve bolted something like 30 extra years onto the human lifespan over the last century, and a healthy 60-year-old today is underwriting a retirement that could run four decades. A liability that long needs a growth engine that long. And the only asset that has reliably outrun inflation over 30-year stretches, through every war, panic, and policy blunder we can point to, is equities.

So look at the Chart again with that in mind. The Boomer sitting at 58% stocks isn’t being naive about risk. She’s matching a 30-year liability with a 30-year asset. The kid at 32%, loading a 13% crypto sleeve that has never funded a real retirement drawdown, is the one taking the bet most people would call reckless if it didn’t have a youthful, contrarian spin.

Now, the kids aren’t crazy to want diversification, and some of these allocations will almost certainly look smart in hindsight. A lot can go right.

But here’s the part that gets lost and something I focus on a lot: the danger in a multi-decade retirement isn’t a bad year. It’s sequence-of-returns risk, the brutal arithmetic of drawing income out of a portfolio while it’s down. Trading the proven long-horizon asset class for illiquid alternatives and a coin that swings +/-70% is exactly the kind of move that wrecks the first ugly decade of a 40-year plan.

If I had to bet, I’d take the Boomers’ instinct over the kids’ enthusiasm. Stay invested in the asset that actually compounds. The job is figuring out how to ride equities through the inevitable drawdowns without selling at the bottom or sending a bunch of your assets to Uncle Sam, That is a risk-management problem, not an asset-allocation one.

I’d say that the young investors got one thing right, though. They’re planning to live a very long time. Allocating more to equities and allowing them to compound over a long investment horizon is in my opinion, still the best way to fund that long life.

Sources: Bank of America press release · Bank of America Institute summary

🚙 Interesting Drive-By’s 🚙

🤔 The VIX Isn’t Broken, It’s Just Being Outplayed - ETF.com’s Dave Nadig and “Vixologist” Jim Carroll argue the fear gauge dozing in the high teens is being drained of signal as risk migrates into same-day 0DTE bets and a plethora of options strategies.

🚪 The World-Building Doors Are Open, Again - Josh Elman marks his arrival at a16z with a manifesto calling AI-first consumer apps the next great build-out, worth reading for the map of where consumer money wants to go as long as you keep one eye on the incentive, since a brand-new VC needs founders convinced the door is open before anyone funds them walking through it.

💰 Longevity and Wealth Transfer Are Making Family Finances More Complex - Rethinking 65 unpacks the 2026 Bank of America Private Bank study of households with $3 million or more, where 67% of heirs aged 21 to 45 say stocks and bonds can no longer beat average returns yet only 33% understand trusts and just 20% of business owners have a documented succession plan, so the great transfer is arriving faster than the planning meant to catch it.

🤔 How Many People Does Synthetic Fertilizer Feed? - Our World in Data’s Hannah Ritchie estimates roughly half the people alive, about 3.5 billion, are fed by crops grown with synthetic nitrogen, which means one 1910 industrial process, Haber-Bosch, sits under the entire population’s food supply as a single point of failure most investors never bother to price.

👀 SpaceX Just Unveiled Their First ‘AI Satellite’ - 24/7 Wall St. details AI1, a 70-meter orbital data center carrying up to 150 kW of compute, where shedding heat in a vacuum is still the unsolved problem and the timing right before the IPO should make any buyer cautious about how much of the valuation now rests on a market that doesn’t exist yet.

👋🏼 Parting Thought

Happy to be back in the Great State of Texas, if only for a few days.

If you have any cool articles or ideas that might be interesting for future Sunday Drive-by’s, please send them along or tweet ‘em (X ‘em?) at me.

Please note that the content in The Sunday Drive is intended for informational purposes only, and is in no way intended to be financial, legal, tax, marital, or even cooking advice. Consult your own professionals as needed. The views expressed in The Sunday Drive are mine alone, and are not necessarily the views of Investment Research Partners.

I hope you have a relaxing weekend and a great week ahead. See you next Sunday...

Your faithful financial provocateur,

-Mike

If you enjoy the Sunday Drive, I’d be honored if you’d share it with others.

If this was forwarded to you, please subscribe and join the other geniuses who are reading this newsletter.