The Sunday Drive - 06/21/2026 Edition [#220]

Musings and Meanderings of a Financial Provocateur

👋🏼 Hello friends! Happy Summer Solstice and Happy Father’s Day to all who celebrate. Now, let’s enjoy another Sunday Drive around the Internet.

🎶 Vibin’

After a week full of chatter about thousands of newly minted millionaires and the world’s first trillionaire, I find it helpful to remember a more humble time when one would peel the foil off a TV dinner and call it a feast.

This week I’m vibin’ to TV Dinners by ZZ Top from 1983 and the Golden Age of MTV. It’s the bluesy throwaway buried on Eliminator, the same record that gave us “Gimme All Your Lovin’.”

Enjoy.

💭 Quote of the Week

“We must avoid a situation where every business venture becomes largely a speculation on the future of monetary policy.”

— Henry Simons

📈 Chart of the Week

Does the Bull Market End With the Boomers?

It’s been a while since we had a demographic-related Chart, so when I ran across this one, I found it interesting enough to write about.

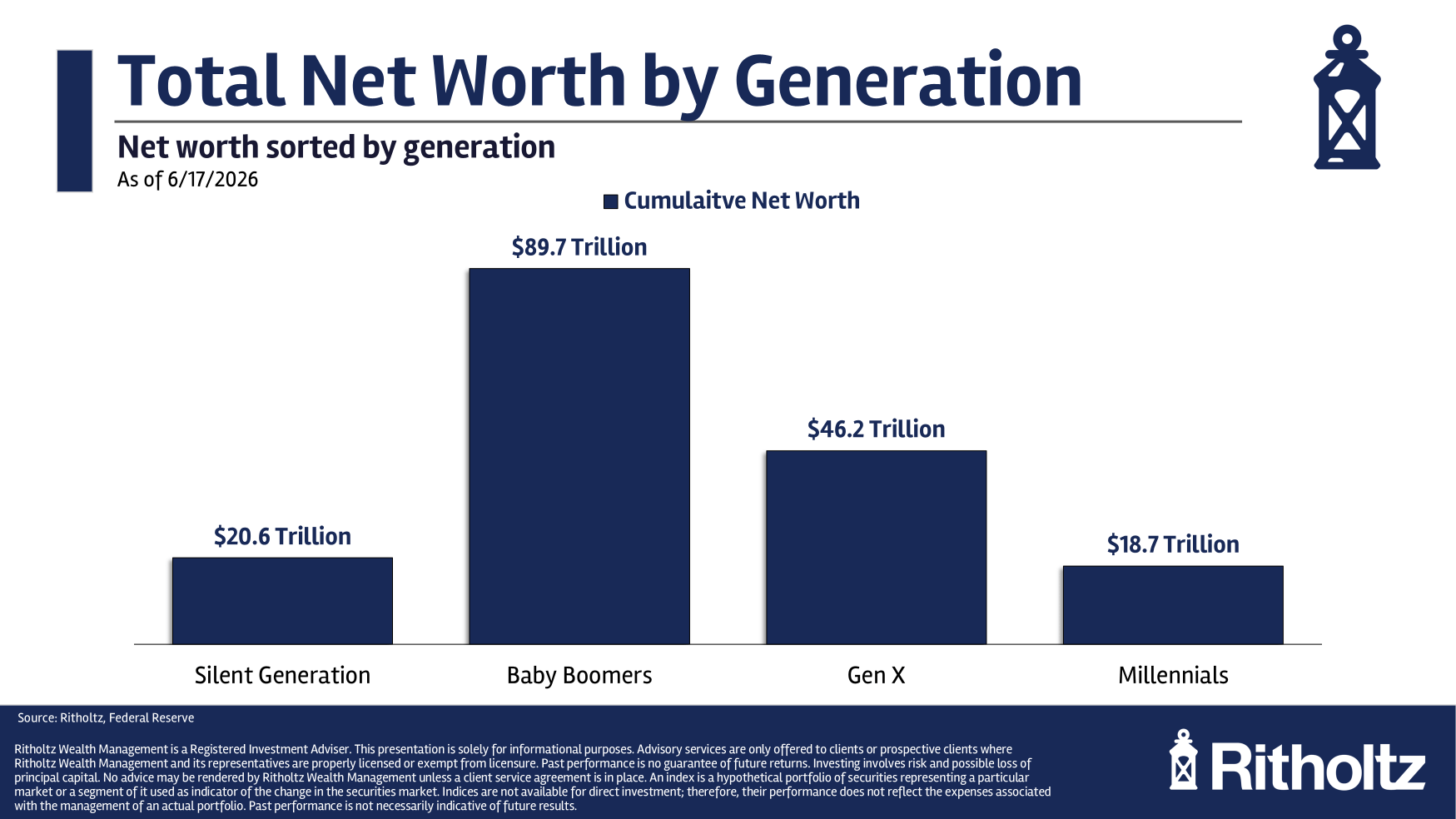

Here’s the worry on the minds of many investors. Baby Boomers hold about $89.7 trillion in net worth, more than the Silent Generation, Gen X, and Millennials combined. Boomers and the generation ahead of them own close to 70% of all the stocks, and they’re retiring. Somewhere between 40 and 50 million of them already are.

So the story writes itself.

The cohort that bought equities for 40 years turns into sellers. Required minimum distributions accelerate. Target-date funds quietly swap stocks for bonds on a fixed glidepath. The relentless bid that Josh Brown described back in 2014, the steady river of 401(k) money that bought every dip without caring about the news, runs in reverse. Call it the relentless ask.

It’s a reasonable theory, but I believe it’s mostly wrong, at least as the reason this bull market ends.

Start with where the money sits. The top 10% of households own about 87% of all stocks. Wealth that concentrated doesn’t get spent down in retirement. It gets bequeathed. A retiree worth eight figures sells a sliver to fund their lifestyle and leaves the rest to compound, because they can’t spend it and don’t need to.

Then there’s longevity, which I believe is an important factor in determining the future of our economy. For a 65-year-old couple today, there’s a 64% chance at least one of them sees their 90s. Retirement now runs 30 years or more. You can’t fund three decades of inflation out of bonds, so Boomers have to keep owning stocks, and most of them will.

And someone is standing on the other side of the trade. There are roughly 73 million Millennials, a slightly larger cohort than the (living) Boomers, hitting their prime earning and saving years right as the Boomers start drawing down their savings. The single largest age group in America is now 33 to 37. They invest earlier and in greater numbers than Boomers did at the same age. The buyers are already here.

One more thing. Demographics are the most forecastable data in all of finance. We’ve known the Boomer cliff was coming for 50 years, and so does the market. Slow, telegraphed, decades-long tides don’t end bull markets. Surprises do.

Which is where the real risk lives, in my opinion. Brown’s word was relentless, not endless. He warned the bid “will suck in the maximum amount of people taking the largest amount of risk just at the point where it will come to an ignominious end.”

I believe the major risk to the equity markets sits somewhere other than a gentle 30-year drawdown.

It’s true that the automatic, price-agnostic flows that smoothed the bull market on the way up could prove just as automatic and just as price-agnostic on the way down, in a market where a handful of names seem to carry the whole thing. That’s the relentless bid’s dark twin, but that’s a forseeable risk and only part of the story.

So does the bull market end with the Boomers? I don’t think so. I think that it ends the way bull markets always end, when corporate earnings growth slows and valuations are stretched and not reflective of that slowdown.

Leaving arguments regarding passive versus active management aside, I believe that fundamentals matter more then flows, even generational ones.

Sources: Federal Reserve, Distributional Financial Accounts (net worth by generation); Ben Carlson, “What Happens to the Stock Market When Baby Boomers Sell?” and “Rich Old People”, A Wealth of Common Sense; Josh Brown, “The Relentless Bid, Explained” and “The Trouble with Relentless Bid Theories”, The Reformed Broker.

🚙 Interesting Drive-By’s 🚙

🤔 The Death of the Summer Job - Larissa Phillips argues the vanishing teen summer job quietly took the grit and competence that busing tables built better than any trip to Europe.

🚀 SpaceX is building a planetary starter kit - Kevin Gee concedes SpaceX’s ~$2.1tn post-IPO cap is “wildly overvalued” by any standard method, then makes the possibility case (not the price case) for a vertically integrated machine whose loops only compound on one balance sheet, which leaves the whole thesis resting on Elon staying the single “integrating core.”

🚀 Tech should live in places that love technology - Adam Singer reads Starbase’s 212-to-6 incorporation vote (97% of an electorate that’s almost entirely SpaceX employees) as proof that atoms-innovation now clusters wherever governance gets out of the way, a clean Silicon Industrials data point whose unspoken risk is that a company town this concentrated is also a single point of failure tethered to one founder and one mission.

🤔 It Is an Active Decision to Go Passive in Equities - JPMorgan AM warns the top 10 names now run ~40% of the S&P 500 (61% of the Russell 1000 Growth), so buying the index is itself an undiversified active bet that yesterday’s winners keep winning, with the firm’s own large-cap forecast at 6.7% a year over the next decade, less than half the last.

📉 xAIr Supply - Michael Green makes the case that the AI bubble is really a financing problem: AI is turning capital-light monopolies into capital-intensive infrastructure firms, so the passive bid that quietly absorbed a decade of buybacks may now have to swallow a wave of equity issuance instead, right as the S&P declined to bend its rules to fast-track SpaceX into the index.

🧠 Good News: Your Brain Isn’t Retiring Anytime Soon - Chip Conley reframes aging as a function of engagement rather than odometer reading, arguing that learning Spanish at 67 or starting a business at 58 is brain maintenance because novelty keeps the wiring elastic.

👋🏼 Parting Thought

Make the most of the longest day.

If you have any cool articles or ideas that might be interesting for future Sunday Drive-by’s, please send them along or tweet ‘em (X ‘em?) at me.

Please note that the content in The Sunday Drive is intended for informational purposes only, and is in no way intended to be financial, legal, tax, marital, or even cooking advice. Consult your own professionals as needed. The views expressed in The Sunday Drive are mine alone, and are not necessarily the views of Investment Research Partners.

I hope you have a relaxing weekend and a great week ahead. See you next Sunday...

Your faithful financial provocateur,

-Mike

If you enjoy the Sunday Drive, I’d be honored if you’d share it with others.

If this was forwarded to you, please subscribe and join the other geniuses who are reading this newsletter.