The Sunday Drive - 06/14/2026 Edition [#219]

Musings and Meanderings of a Financial Provocateur

👋🏼 Hello friends! Let’s enjoy another Sunday Drive around the Internet.

🎶 Vibin’

Well, the SpaceX IPO finally happened this week...

I feel like this is a seminal moment in the history of capital markets, the ramifications of which have yet to be revealed to us. But they will eventually, and I believe they will be significant.

For no particular reason (h/t Forest Gump), this week I’m vibin’ to The Joker by the Steve Miller Band from 1973. The “space cowboy” line has been stuck in my head for days.

💭 Quote of the Week

“Until you’re ready to look foolish, you’ll never have the possibility of being great.”

— Cher

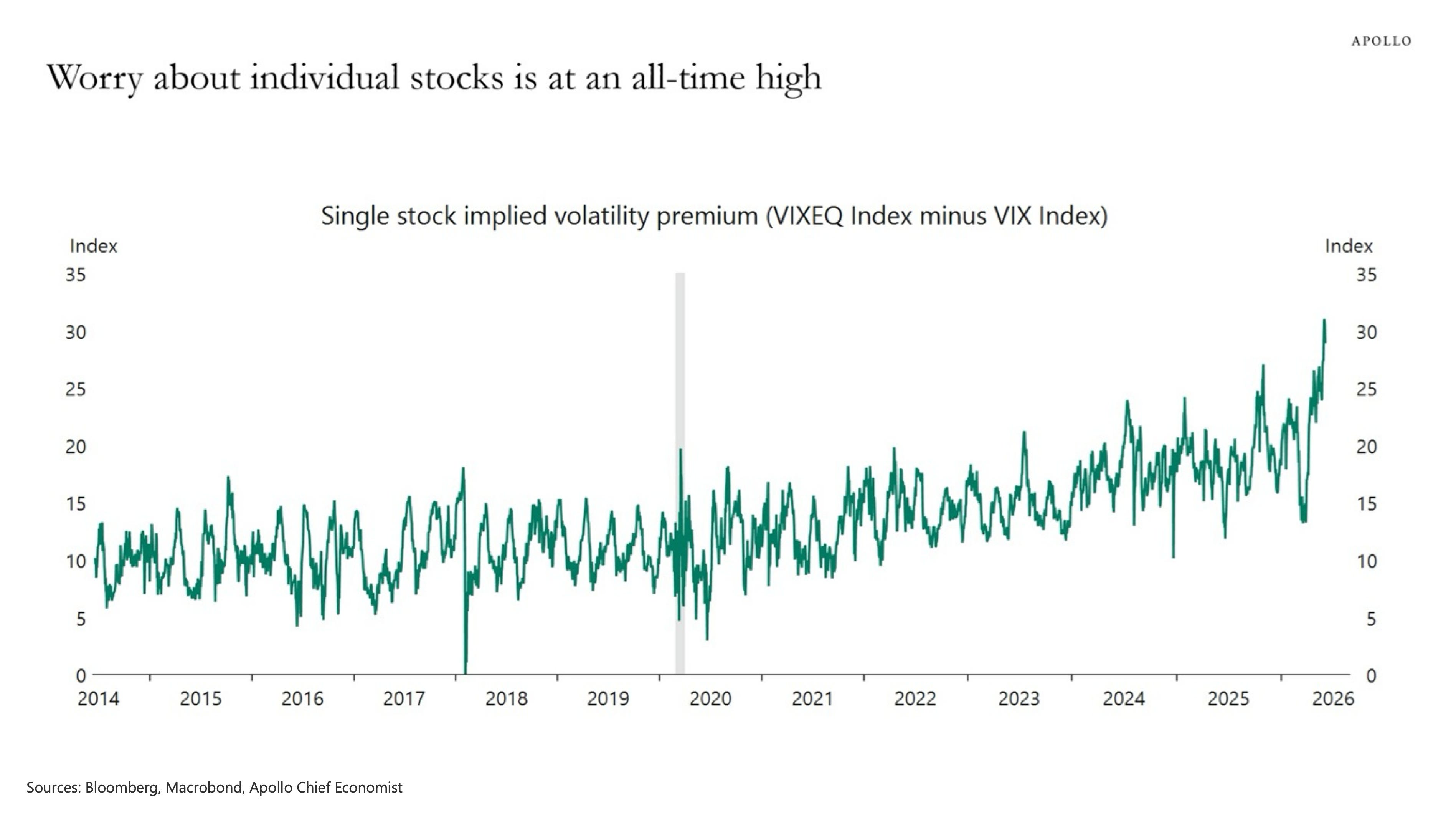

📈 Chart of the Week

The Quiet in the Index Is the Real Risk

This week’s Chart contains a one-line caption: Worry about individual stocks is at an all-time high. I think the caption has the story backwards.

The line in the Chart shows the spread between two fear gauges.

The VIX measures how nervous traders are about the whole market, the S&P 500, over the next month. Think of it as the price of insurance on the index.

The VIXEQ does the same thing for individual stocks and averages them weighted by market cap. Subtract one from the other and you get how much more it costs to insure a single name than the index. That gap just hit about 30, the widest in more than a decade, up from a long-run norm closer to 10.

Apollo’s Chief Economist, Torsten Slok, sees that as fear of individual companies. I mostly see it as plumbing.

Implied volatility is a major determinant of how options are priced. And prices come from supply and demand, not feelings. Two different things are happening in two different options markets, in my view.

On single stocks, there’s a flood of buying. Retail traders piling into call options on Nvidia and other tech names before earnings. Same-day options on whatever name is hot that week. Dealers forced to buy stocks on the calls they’ve written in order to keep their hedges flat.

All that demand bids up the price of single-stock options, and that shows up as high implied volatility. Some of it is worry. A lot of it is gambling.

On the index, the opposite is happening. There’s now a giant business built around selling index options for income. Covered-call ETFs, buffer products, pensions writing calls every month. All that selling pushes the price of index insurance down, and that shows up as a muted VIX.

In my opinion, the spread is so wide because one market is being bought hard and the other is being sold hard. Worry is part of it, yes. The mechanics of the options market could be most of it.

Now the part that actually matters for investors. The risk worth watching sits on the calm side of the ledger. A VIX at 15 in a market this concentrated, where a handful of stocks carry the whole thing, is not the same animal as a 15 in a broad and participative market. The steady option selling that holds the VIX down works right up until it doesn’t.

That spread will narrow at some point, perhaps significantly. It always has. There are two ways it can get there. Single-stock vol could fall, but I doubt it, because the options-market shifts driving it look structural rather than temporary.

Or... Index vol rises to meet it. That’s the path I’d bet on, and the trigger could be almost anything that wakes the index up from a risk perspective: a crack in one of the megacaps, a rate or inflation scare (or both), a credit event nobody sees coming.

A muted VIX is a sign of confidence, but when that remains the case for too long, confidence becomes complacency. The quiet you see in the volatility of the index is the thing most worthy of worry.

Sources: Apollo Chief Economist (Torsten Slok), “Worry about individual stocks is at an all-time high” (data via Bloomberg, Macrobond); Mandy Xu, Earnings Angst Drives VIXEQ-VIX Index Spread to Record High, Cboe, Oct. 13, 2025; There’s a record disconnect unfolding in the trading pits right now, CNBC, May 29, 2026

🚙 Interesting Drive-By’s 🚙

📉 The Lowest Consumer Sentiment EVER - Ben Carlson on a head-scratcher: sentiment just hit its lowest in the survey’s 75 years, below the GFC and Covid, even with stocks near highs and unemployment at 4.3%.

🤔 If You Can’t Get a Job Today, It’s Your Fault - Auren Hoffman argues the entry-level market isn’t soft (4.3% unemployment, junior hiring up 8.7% at big firms) but mismatched, and what gets you hired now is something you built, not the college brand.

🚀 It’s Hardware’s Turn to Eat the World - Stephen McBride coins “Silicon Industrials,” firms like Tesla, SpaceX, and Anduril that bolt a software brain onto real machines to claim the $93 trillion physical economy that software never touched.

🤔 The AI Boom vs. the Dot-Com Boom - A clear-eyed look at what broke the 2000 bubble and where AI rhymes.

🤔 Quantum Computing: Hype or the Real Deal? - Michael Lebowitz cuts past the 13,000x-faster Willow headlines to the number that governs the timeline: it still takes 1,000 to 10,000 physical qubits to make one reliable one, so a useful machine sits a decade out.

🤔 Venture Capital’s Fourth Turning - Kyle Harrison lands on the number every LP should be staring at: $3.2 trillion of unrealized value trapped in private markets with exits nowhere in sight, which is why 72% of LPs are already cutting allocations.

👋🏼 Parting Thought

Today we celebrate the 249th birthday of our American Flag. 🇺🇸

If you have any cool articles or ideas that might be interesting for future Sunday Drive-by’s, please send them along or tweet ‘em (X ‘em?) at me.

Please note that the content in The Sunday Drive is intended for informational purposes only, and is in no way intended to be financial, legal, tax, marital, or even cooking advice. Consult your own professionals as needed. The views expressed in The Sunday Drive are mine alone, and are not necessarily the views of Investment Research Partners.

I hope you have a relaxing weekend and a great week ahead. See you next Sunday...

Your faithful financial provocateur,

-Mike

If you enjoy the Sunday Drive, I’d be honored if you’d share it with others.

If this was forwarded to you, please subscribe and join the other geniuses who are reading this newsletter.

I hadn't understood that the explosion in covered call ETFs caused the VIX to be artificially low.