The Sunday Drive - 05/24/2026 Edition [#216]

Musings and Meanderings of a Financial Provocateur

👋🏼 Hello friends! Let’s enjoy another Sunday Drive around the Internet.

🎶 Vibin’

The SpaceX IPO is coming. I don’t think it will take long for the stock to be included in the S&P 500 and other indexes and there it will stay. Once you’re in the index, you can check out any time you like, but you can never leave.

This week I’m vibin’ to the Eagles and Hotel California.

💭 Quote of the Week

“Investing isn’t a game of analysis; it’s a game of meta-analysis. We can’t predict the future with any degree of accuracy. But market valuations reveal the distribution of other people’s forecasts, and we look for places where optimism or pessimism have become extreme.”

— Dan Rasmussen

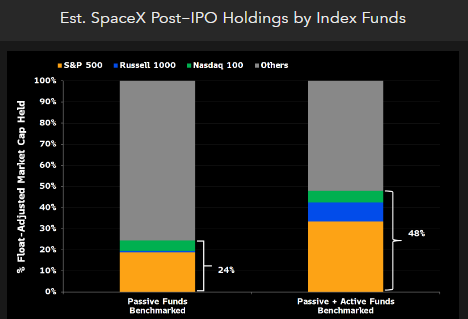

📈 Chart of the Week

A Different Type of Supply Side Economics

This week’s Chart highlights something I’ve been thinking a lot about lately, the SpaceX IPO.

The numbers are pretty straightforward: somewhere between 24% (passive funds only) and 48% (passive plus benchmarked active funds) of SpaceX’s entire post-IPO float will end up in the hands of index funds.

The immediate reaction is to say: great for SpaceX’s stock price. And it probably will be. But the more interesting story, and the one getting little attention at the moment, runs in exactly the opposite direction.

The Concentration Irony

Over the couple of decades, the passive investing boom did something remarkable to the S&P 500. It concentrated it. Every dollar flowing into SPY or IVV gets allocated to every member of the index weighted by float-adjusted market cap. The biggest companies attract the most passive dollars; the more passive dollars they attract, the bigger they get; the bigger they get, the more passive dollars they attract. This is how the “Magnificent Seven” — Apple, Microsoft, NVIDIA, Alphabet, Amazon, Meta, and Tesla — came to represent roughly 32% of the entire S&P 500 heading into 2026.

The passive investing machine built the Mag-7 concentration. It is now, mechanically, about to start unwinding a piece of it, but not because anyone changed their view on Apple’s earnings power or NVIDIA’s AI dominance. It’s because SpaceX is going public and will likely be added to the S&P 500 and other indexes on an accelerated timeline.

The Mechanics

Index funds don’t hold cash. They’re fully invested, always. When SpaceX gets added to the S&P 500, a fund tracking the index must sell a pro-rata slice of every existing holding to fund the SpaceX purchase. There is no other source of capital. The Mag-7 names, being the largest holdings, bear the largest dollar amount of that selling; completely mechanical, completely indifferent to fundamentals, happening across hundreds of funds simultaneously.

Let’s consider the magnitude of this.

SpaceX’s last reported secondary transaction valued the company at approximately $350 billion in late 2024. Since then, Starlink’s subscriber base has continued growing, Starship has matured from spectacle to operational vehicle, and the AI infrastructure narrative has made orbital data centers a serious capital expenditure conversation rather than a science fiction one. A $500 billion IPO valuation is conservative relative to the bull case.

Elon Musk owns approximately 42% of SpaceX. Apply a 25% float assumption at IPO, constrained by Musk’s stake and standard lockup structures, and you get roughly $125 billion in float-adjusted market cap entering the index. Against a total S&P 500 float of approximately $45 trillion, SpaceX arrives at about 0.28% weight.

Every existing member gets diluted by that 0.28%. For the Mag-7, at their approximate current market capitalizations, that translates to roughly $9 billion in forced selling on Apple, $8 billion each on Microsoft and NVIDIA, $7 billion on Amazon, $6 billion on Alphabet, $4.5 billion on Meta, and $3 billion on Tesla — approximately $46 billion in forced, fundamentals-indifferent selling on the Mag-7 from S&P 500 index funds alone.

The Nasdaq 100 Multiplier

Now add the Nasdaq 100. If SpaceX lists on Nasdaq, which is probable, and the math compounds. The Nasdaq 100 is even more concentrated in tech than the S&P 500, so SpaceX’s inclusion weight would be larger, and the names absorbing the pro-rata selling are, again, essentially identical to the Mag-7. QQQ alone runs over $320 billion in AUM. Between S&P 500 rebalancing, Russell 1000 rebalancing, Nasdaq 100 rebalancing, and the benchmarked active funds included in the Chart’s 48% figure, total forced selling across the Mag-7 could approach $80–100 billion spread over a multi-week inclusion window.

I don’t believe this will crater the Mag-7. But it is a meaningful, durable headwind.

Float Creep: The Slow Bleed

Here’s what makes this a multi-year story rather than a one-time event. Musk’s stake doesn’t disappear at the IPO, it gets locked up and gradually freed. As the lockup tranches expire over the 12–24 months following inclusion, SpaceX’s float-adjusted market cap grows, its index weight increases, and passive funds must continue buying more SpaceX, funded by continued selling of everything else. This is a slow, structural bleed disproportionately impacting the Mag-7, one lockup expiration at a time, for years.

Tesla is perhaps the most instructive precedent.

Added to the S&P 500 on December 21, 2020 at a market cap of roughly $650 billion, Tesla triggered an estimated $70–80 billion in passive buying. The stock surged approximately 70% in the weeks leading into its inclusion as front-runners positioned early. What received far less attention was the quiet, sustained pro-rata selling across every other large-cap holding, including several names now sitting in the Mag-7, that followed in the months after.

The SpaceX dynamic isn’t identical: Tesla was already public and had years of established price discovery before index inclusion. SpaceX’s IPO and index admission will likely compress into a much shorter window, concentrating the dislocation. But the mechanics are the same.

The Takeaway: The passive investing machine spent decades concentrating the S&P 500 into seven names. It is about to spend the next several years mechanically diluting them, dollar for dollar, to make room for the next one. And the ones after that, namely OpenAI and Anthropic.

That’s not necessarily a reason to sell the Mag-7. It is a reason to think carefully about what multiple you’re paying for businesses whose largest source of structural demand will have permanent new competitors for those same passive dollars.

Sources: Bloomberg, SPGlobal, Wall Street Journal, Yahoo Finance, YCharts.

🚙 Interesting Drive-By’s 🚙

👀 Tracking the Singularity: Week of May 11th — Peter Diamandis on Anthropic’s 80x Q1 growth, Elon handing over Colossus 1, and the case that AI demand goes to infinity. “The Singularity has a revenue problem (too much demand).”

🚀 AI Data Centers in Space Are No Joke — James Pethokoukis on the SpaceX IPO, Starship V3, and the case that full reusability could make orbital data centers a real piece of AI infrastructure rather than a sci-fi sideshow.

🤔 Artificial Manipulation — Dror Poleg’s counter to the “more intelligence solves everything” narrative: we usually know what to do, we just don’t feel like doing it. The scarce resource isn’t intelligence — it’s coordination and consent — and AI’s real power may be persuading and enforcing at a scale no human institution ever could.

📊 How America Turned Against AI According to the Poll Data: A (Very Big) Compilation — Alberto Romero stitches together every major poll on AI sentiment — Gallup, Pew, Change Research, WaPo-Schar, Marquette, Morning Consult, NBC, Heatmap — and they all point the same way. 71% oppose a datacenter in their area (now more opposed than nuclear plants), 57% say AI’s risks outweigh the benefits, the partisan gap has collapsed, and Change Research clocked a 40-point net swing in a single year. $156B in disrupted projects, 188+ opposition groups, 300+ state bills. Sobering reading for anyone long the hyperscalers — or living near one.

💰 Scott Galloway had the audience. Here’s what he came for. — Two months into his Substack run, Prof G walks through the math out loud: $20M of podcast revenue trades at a 2–3x multiple, but recurring subscription ARR trades at 4–6x — and the whole company re-rates higher when subscription is growing faster than the core ad business. He’s targeting $1M ARR on Substack by year-end. Also drops a contrarian AI call worth the price of admission: “AI, from a valuation standpoint and a labor destruction standpoint, has been vastly overhyped… I think we’re going to see a similar drawdown as the dot-com implosion. I’ve been to this movie before.” A clinic on platform economics, exit multiples, and where your margin is somebody else’s opportunity.

🎓 How to Start a Career When AI Is Doing Your Entry-level Job — Katie Parrott on the squeeze hitting today’s grads: Stanford’s Digital Economy Lab clocks a 13% drop in employment for 22-to-25-year-olds in AI-exposed jobs since late 2022, even as older workers in the same roles held steady. Her four-part survival kit for the Class of 2026 — chase problems not professions, pick one craft and protect it from automation, make things before anyone asks, and stand up your own AI career coach — is the most practical thing I’ve read on entry-level reinvention. A useful counterpoint to Galloway’s view (one drive-by up) that the labor apocalypse is mostly a fundraising technique. Both can be true at once: real damage at the bottom rung, hype at the top of the cap stack.

📚 Kids should learn how to short stocks — Brent Sullivan’s read: tax-aware long/short (130/30, 200/100, etc.) has now crossed $150 billion in AUM, which means the days of advisors and end-clients waving off shorting as “too complicated for normal portfolios” are over. If you’re hiring a manager in this space — or being hired as one — you need the mechanics in your bones. Sullivan points to a free online resource that teaches the next generation how shorts actually work.

👋🏼 Parting Thought

All gave some. Some gave all. 🇺🇸

If you have any cool articles or ideas that might be interesting for future Sunday Drive-by’s, please send them along or tweet ‘em (X ‘em?) at me.

Please note that the content in The Sunday Drive is intended for informational purposes only, and is in no way intended to be financial, legal, tax, marital, or even cooking advice. Consult your own professionals as needed. The views expressed in The Sunday Drive are mine alone, and are not necessarily the views of Investment Research Partners.

I hope you have a relaxing weekend and a great week ahead. See you next Sunday...

Your faithful financial provocateur,

-Mike

If you enjoy the Sunday Drive, I’d be honored if you’d share it with others.

If this was forwarded to you, please subscribe and join the other geniuses who are reading this newsletter.