The Sunday Drive - 05/10/2026 Edition [#214]

Musings and Meanderings of a Financial Provocateur

👋🏼 Hello friends!

It’s Mother’s Day, so let us celebrate her… and enjoy another Sunday Drive around the internet.

🎶 Vibin'

Another week of solid corporate earnings reports. Another week of fairly ambiguous geopolitical non-action in the Middle East. Another week of generally strong economic numbers.

…and the markets kept on Truckin’.

The vibe this week just sorta self-identified. Enjoy this run while it lasts.

💭 Quote of the Week

“If you hear a voice within you say ‘you cannot paint,’ then by all means paint, and that voice will be silenced.”

— Vincent van Gogh

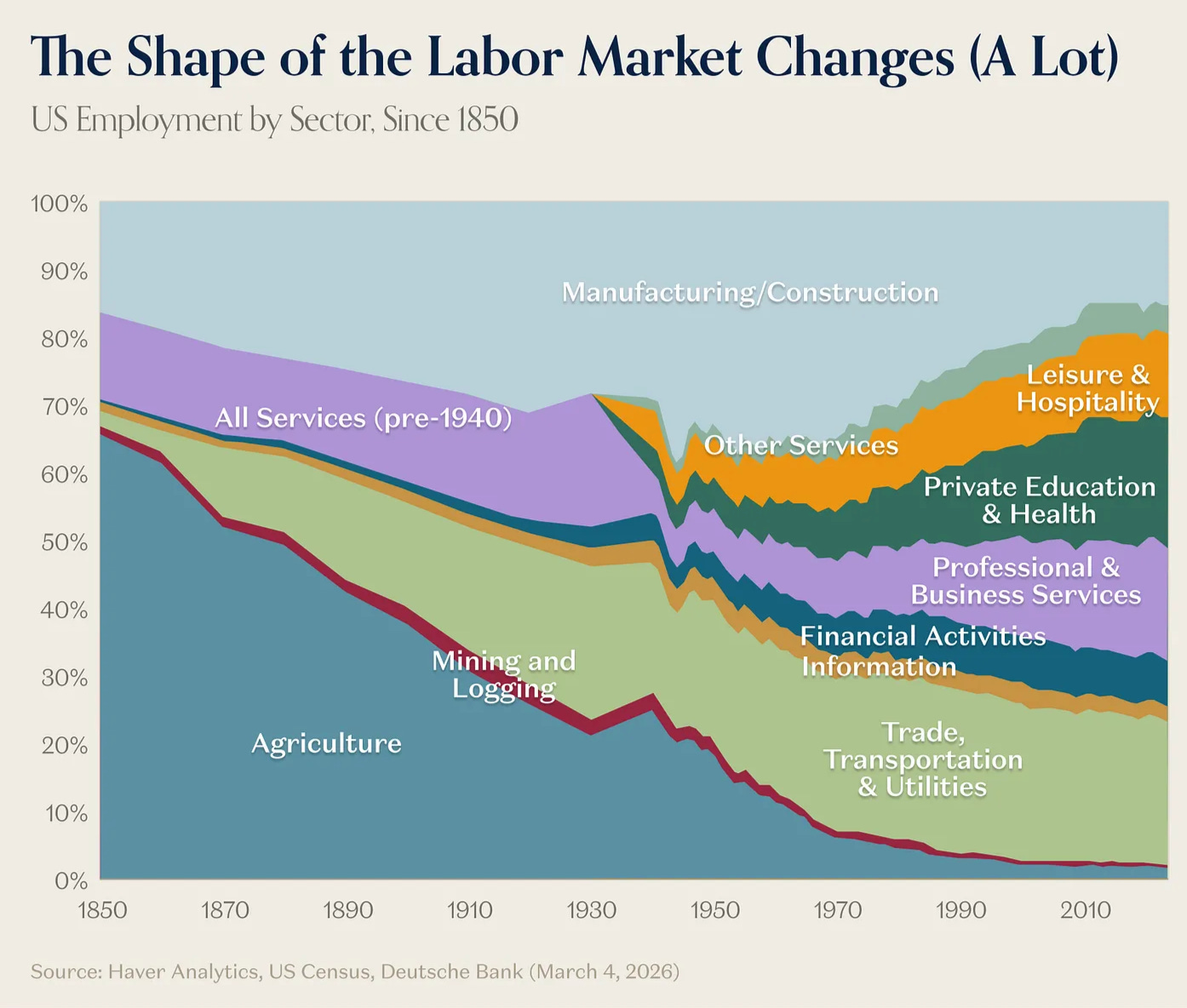

📈 Chart of the Week

There Is No “Lump of Labor”

Friday’s April employment report came in well above expectations: nonfarm payrolls rose +115,000 versus a consensus estimate of just +55,000, while the unemployment rate held steady at 4.3%. March was revised up to +185,000 — the first back-to-back monthly gains in nearly a year, and a meaningful tell that the so-called “low-hire, low-fire” labor market may finally be finding its footing again.

You wouldn’t know any of this from the discourse.

Open your media feeds and you’ll find an endless parade of AI Doomers warning that this is the calm before the storm; that white-collar work is about to be hollowed out, that entry-level roles are already disappearing, and that a “permanent underclass” is being engineered as we speak. The AI Job Apocalypse now seems to be its own sub-genre on Substack, YouTube, and other media outlets.

I’m not buying it. And frankly, neither is the data.

This week’s Chart, courtesy of Deutsche Bank, by way of Haver Analytics and the U.S. Census, does a lot to dismantle the current AI doom narrative.

It shows the composition of U.S. employment by sector going back to 1850.

In 1850, roughly two-thirds of American workers were in agriculture. By 2025, that figure was about 2%. Mining, logging, and even manufacturing followed similar arcs.

And yet through every wave of disruption: the tractor, the assembly line, electrification, the PC, the internet, the U.S. economy didn’t run out of jobs. It ran out of certain jobs, and then created entirely new categories to take their place.

This is the “lump-of-labor fallacy“, the assumption that there is a fixed amount of work to be done, and that anything (or anyone) capable of doing more of it must necessarily leave less for the rest of us.

It’s the same premise that fueled Luddite anxieties in 1811, Keynes’s failed 1930 prediction of a 15-hour workweek, and the AI panic of today. It defies everything we know about how humans, markets, and economies actually behave.

When the cost of a key input collapses, demand expands. Quality rises. New products become viable. Whole new industries get built. Jevons Paradox, in a nutshell: demand growth driven by lower cost supply of inputs.

What’s striking is that the current data is already confirming all of this.

The Yale Budget Lab’s April report concluded that AI’s impact on the labor market thus far “largely reflects stability, not major disruption.”

A recent Atlanta Fed working paper found that more than 90% of firms estimate no impact on employment from AI over the past three years.

Goldman’s analysis suggests AI augmentation effects more than offset substitution effects. On corporate earnings calls, mentions of AI-as-augmentation are outpacing AI-as-substitution by roughly 8 to 1.

Meanwhile, software engineering job postings are inflecting upward. AI-related capex has triggered the biggest run on skilled trades and data center construction labor in a generation.

New business formation is running at a pace that closely correlates with AI adoption. The scoreboard is decidedly not the one the doomers have been forecasting.

The Takeaway: The shape of the labor market always changes. That’s the whole story this week’s Chart tells, and it has been the story for 175 years running. AI will eliminate some tasks, compress some roles, and inflict real pain on workers caught in the middle of the transition; that part is genuine, and it deserves to be taken seriously, particularly with respect to retraining and displacement support.

But the leap from “some jobs will disappear” to “permanent mass unemployment” requires you to assume that human ambition, curiosity, and wants are about to suddenly stop expanding. They aren’t. They never have.

There is no fixed lump of labor. There never was. And if Friday’s jobs report is any indication, the labor market is quickly and quietly doing exactly what it has done since 1850 — remaking itself, one sector at a time.

Sources: BLS Employment Situation – April 2026; Deutsche Bank / Haver Analytics / U.S. Census (March 4, 2026); a16z News – David George, “The ‘AI Job Apocalypse’ Is a Complete Fantasy” (May 6, 2026); Yale Budget Lab (April 16, 2026); Federal Reserve Bank of Atlanta Working Paper 2026-3.

🚙 Interesting Drive-By's 🚙

🤔 The Longevity Revolution is Here

📈 The Marks Aren’t High Enough - Ruminations on Equity Values, Public and Private

💰 Wall Street Readies Data Center IPOs as AI-Linked Debuts Surge

💸 AI’s Looming Talent Retention Problem

👋🏼 Parting Thought

To all the mother’s out there, especially the mother of my children… Thank you. ❤️

If you have any cool articles or ideas that might be interesting for future Sunday Drive-by's, please send them along or tweet 'em (X ‘em?) at me.

Please note that the content in The Sunday Drive is intended for informational purposes only, and is in no way intended to be financial, legal, tax, marital, or even cooking advice. Consult your own professionals as needed. The views expressed in The Sunday Drive are mine alone, and are not necessarily the views of Investment Research Partners.

I hope you have a relaxing weekend and a great week ahead. See you next Sunday...

Your faithful financial provocateur,

-Mike

If you enjoy the Sunday Drive, I'd be honored if you'd share it with others.

If this was forwarded to you, please subscribe and join the other geniuses who are reading this newsletter.