The Sunday Drive - 05/03/2026 Edition [#213]

Musings and Meanderings of a Financial Provocateur

👋🏼 Hello friends! Let’s enjoy another Sunday Drive around the internet.

🎶 Vibin'

This past week saw continued strong reported earnings and outlooks from many companies, including some of the largest tech and AI related names. That seemed to outweigh concerns about a divided Fed that doesn’t seem inclined to lower interest rates any time soon, continued uncertainty in the Middle East, and higher energy prices. The markets, in particular the S&P 500, continued to make new all-time highs.

So, this week, I’m vibin’ to the 5th Dimension’s 1968 hit, “Up, Up and Away.” ‘Cuz why not?

💭 Quote of the Week

“Once you replace negative thoughts with positive ones, you’ll start having positive results”

— Willie Nelson

📈 Chart of the Week

Good Things Come in Small Packages

For the better part of the past decade, the story of the U.S. equity market has been written almost exclusively by the largest companies on the planet. The Magnificent 7. The hyperscalers. The trillion-dollar club. Meanwhile, the smallest, scrappiest, most speculative names, the micro-caps, were left for dead.

The narrative was clean, simple, and seemingly bulletproof: small caps are uninvestable, micro-caps even less so. Too much floating-rate debt. Too little profitability. Too vulnerable to AI displacement. Too irrelevant in a world where capital concentrates relentlessly at the top.

The eulogies were premature.

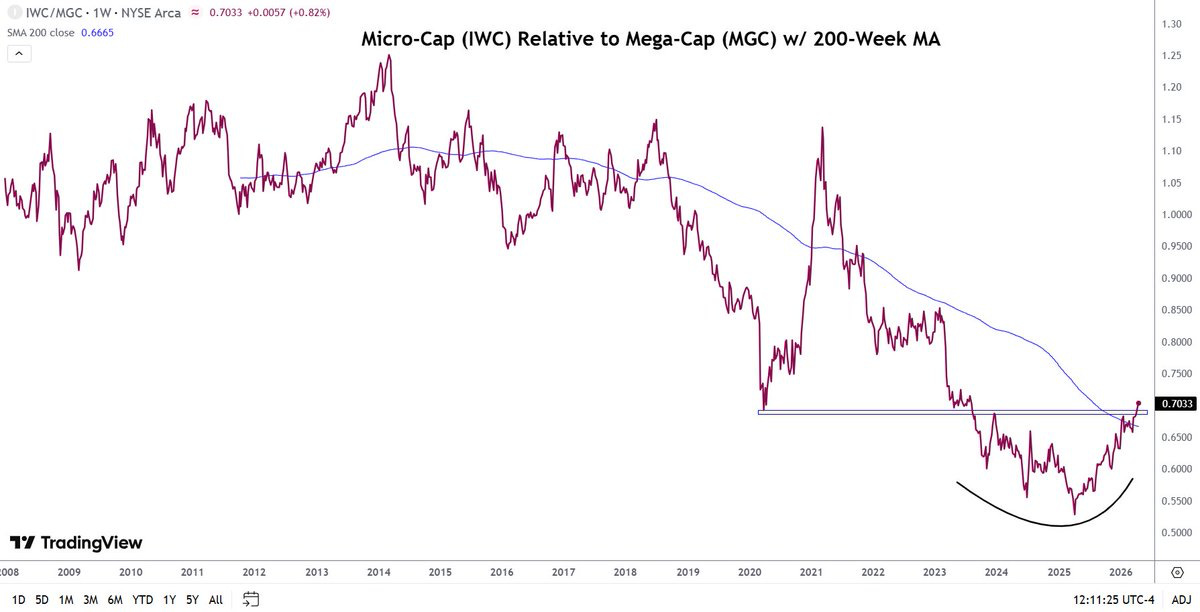

This week’s Chart shows the relative performance of iShares Micro-Cap ETF (IWC) to Vanguard Mega-Cap ETF (MGC) going back to 2008, with the 200-week moving average overlaid. On Friday, IWC printed a new all-time high in absolute terms — and the relative ratio against mega-caps reached its highest level in more than three years.

We also see from the Chart that micro-caps have reclaimed a couple of very important technical levels: the 200-week moving average, beneath which they had been trapped since early 2020 and the pivot lows from the COVID-era washout. That’s the kind of breakout that reverses what has been a structurally negative relative trend for nearly half a decade. Five years of “small is dead” sentiment, finally may be undone.

Now consider the market structure problem.

The Magnificent 7 alone command a combined market cap measured in the tens of trillions of dollars. The entire IWC universe, every micro-cap name combined, is a rounding error by comparison.

When sentiment shifts, when allocators decide they’ve been too concentrated for too long, when active managers go hunting for differentiated returns, all of that capital has to squeeze through a doorway roughly the width of a turnstile to get to the other side.

There simply isn’t enough float to absorb the flow without moving prices, sometimes violently. The crowd is large. The doorway is narrow. Math does the rest.

This is precisely why micro-cap leadership matters out of proportion to the segment’s economic weight. Micro-caps don’t lead when investors are scared. They lead when investors are willing. Their outperformance is the financial equivalent of betting the longshot at Saratoga, it only happens when the crowd genuinely believes in the upside.

The cross-asset signals appear to confirm investors’ risk-on sentiment. Credit spreads remain fairly tight. High yield seems firm. Volatility remains generally contained. This market seems to be deliberately expanding its risk appetite outward, from the largest names to the smallest.

The Takeaway: The “small caps are uninvestable” consensus was crowded, comfortable, and now appears to be wrong (for now). Over the year or so, I’ve mentioned on several occasions of my Goldilocks scenario whereby equities overall do okay but the participation broadens out. That appears to be happening, maybe even accelerating. Combine this with a structural mismatch between the size of the trade and the size of the asset class, and you have the makings of a move that doesn’t have to be subtle to be sustained. Good things sometimes really do come in small packages.

🚙 Interesting Drive-By's 🚙

📈 Jobs Are Dead. Long Live the $10mm Niche

💰 Long Term Money - from Morgan Housel

👀 You Are the Most Expensive Model

👋🏼 Parting Thought

If you have any cool articles or ideas that might be interesting for future Sunday Drive-by's, please send them along or tweet 'em (X ‘em?) at me.

Please note that the content in The Sunday Drive is intended for informational purposes only, and is in no way intended to be financial, legal, tax, marital, or even cooking advice. Consult your own professionals as needed. The views expressed in The Sunday Drive are mine alone, and are not necessarily the views of Investment Research Partners.

I hope you have a relaxing weekend and a great week ahead. See you next Sunday...

Your faithful financial provocateur,

-Mike

If you enjoy the Sunday Drive, I'd be honored if you'd share it with others.

If this was forwarded to you, please subscribe and join the other geniuses who are reading this newsletter.