The Sunday Drive - 04/19/2026 Edition [#211]

Musings and Meanderings of a Financial Provocateur

👋🏼 Hello friends! Let’s enjoy another Sunday Drive around the internet.

🎶 Vibin'

This past week, equity markets continued to recover from the March lows amid the seemingly improved situation in the Middle East (subject to change at any moment, of course).

So I thought an upbeat bouncy tune would be the right vibe for this week. I believe that The Heart of Rock & Roll by Huey Lewis & The News fits the bill quite nicely. I hope you’ll agree.

💭 Quote of the Week

“A life is not important except in the impact it has on other lives.”

— Jackie Robinson

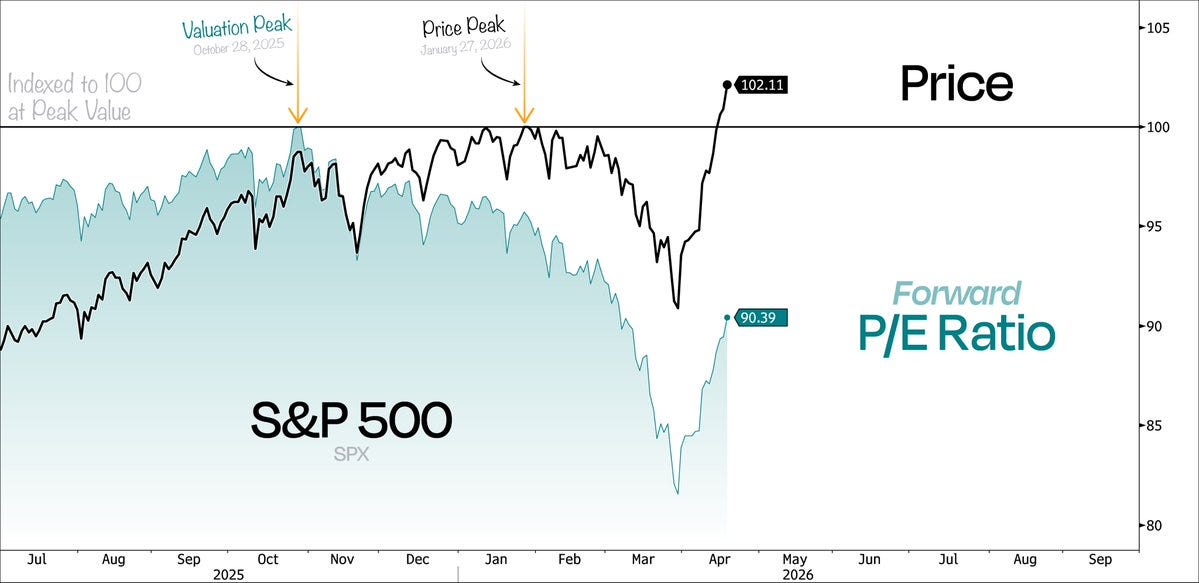

📈 Charts of the Week

Similar Setup, Very Different Story

The S&P 500 is back at all-time highs. You’d be forgiven for assuming nothing has changed. But look at this week’s two Charts above and you’ll see something worth paying attention to: price is essentially where it was, but the forward P/E is not.

That gap is the whole story this week.

The first Chart tells it visually. It shows the S&P 500 and forward Price/Earnings ratio, both indexed to 100 for comparability. The S&P 500 peaked on January 27th, 2026. The forward P/E peaked even earlier, back on October 28th, 2025. Today, the market is at an all time high. But the forward P/E? It’s roughly 10% below the October peak. The market has recovered its price losses, but it has not recovered its valuation losses. That’s not a contradiction. It might actually be the most important sentence in this week’s piece.

The math is simple: if price is flat-to-up but the P/E multiple is down, earnings estimates must have moved higher. And they have, significantly.

Heading into Q4 2025, the forward 12-month P/E stood at 22x, above both the 5-year average of 20x and the 10-year average of 19x. Today, it sits at 19.5x, roughly splitting the difference. That’s a meaningful compression in the multiple, driven almost entirely by rising earnings expectations.

Where are those estimate revisions coming from?

Most of the upward revisions has been concentrated in two sectors: Information Technology and Energy. IT has seen the largest dollar-level increase in earnings of all eleven sectors since December 31st, with Energy a close second. Within technology, the move has been sharp, driven largely by semiconductor names like Micron and Oracle, whose AI-related earnings revisions have been nothing short of extraordinary. The semiconductor buildout underpinning AI infrastructure doesn’t seem to be slowing down, and the earnings estimates are reflecting that reality.

For Q1 2026, Information Technology is projected to report earnings growth of +45.0% year-over-year, with Materials at +24.2% and Financials at +15.1%. Those are not small numbers.

The laggard? Health Care. The sector is expected to report earnings decline of -9.8% in Q1 2026, though the bulk of that drag traces back to a Merck one-time acquisition charge — ex-Merck, the sector’s growth rate would be closer to +2.8%. Energy has been the wild card, whipsawing on geopolitical developments and oil price volatility.

Here’s the comparison that really matters.

When the S&P 500 recovered to all-time highs in late June 2025, following the spring’s tariff-driven selloff, the forward P/E sat at approximately 22.5x. The April 8th, 2025 low had carried a forward P/E of 18.0x, meaning the entire recovery was accompanied by a dramatic 24% expansion in the market’s earnings multiple.

This time around, the script is different. The market has recovered on earnings growth. That should, or at least could, prove to be a more durable foundation.

The asterisk is that forward estimates are exactly that: forward. Analysts are currently calling for full-year 2026 S&P 500 earnings growth of 17.4%. That’s an ambitious number in an environment where tariffs, geopolitical uncertainty, and slowing consumer demand could all have an impact. Guidance this earnings season — not the Q1 headline numbers — will tell us whether those estimates are grounded in reality or still anchored to a world that no longer exists.

The Takeaway: The market’s return to all-time highs is being powered by earnings revisions, not multiple expansion. Compared to the June 2025 recovery, today’s valuation setup is meaningfully more attractive, but the quality of those forward estimates is now the central question. Watch what companies say about the next six months. That’s where the real data lives.

Sources: FactSet Earnings Insight | RBC Wealth Management | Investing.com | IG International

🚙 Interesting Drive-By's 🚙

🤔 The Organizational Singularity Is Here

💡 The Trillion-Dollar Perception Gap Between Silicon Valley and Normal People

👀 Collab Holdings - A different approach to private equity

😡 AI Will Be Met With Violence, and Nothing Good Will Come of It

👋🏼 Parting Thought

2026 has been a tough year for guys named Claude.

If you have any cool articles or ideas that might be interesting for future Sunday Drive-by's, please send them along or tweet 'em (X ‘em?) at me.

Please note that the content in The Sunday Drive is intended for informational purposes only, and is in no way intended to be financial, legal, tax, marital, or even cooking advice. Consult your own professionals as needed. The views expressed in The Sunday Drive are mine alone, and are not necessarily the views of Investment Research Partners.

I hope you have a relaxing weekend and a great week ahead. See you next Sunday...

Your faithful financial provocateur,

-Mike

If you enjoy the Sunday Drive, I'd be honored if you'd share it with others.

If this was forwarded to you, please subscribe and join the other geniuses who are reading this newsletter.