The Sunday Drive - 04/12/2026 Edition [#210]

Musings and Meanderings of a Financial Provocateur

👋🏼 Hello friends! Time for another Sunday Drive around the internet.

Before we start, I want to address an omission from the 208th edition published two weeks ago. The March 29th edition marked the 4 year anniversary of the Sunday Drive. I am grateful to all of you who have come along on this journey with me. Let’s keep going…together.

🎶 Vibin'

This week’s vibe has a double meaning.

Next month, my whole family will be reunited once again in Saratoga Springs, NY. After nearly two years away, the daughter-bear is moving back home and we couldn’t be more excited.

Also, this past week, the entire team at Investment Research Partners gathered in Charleston, SC for our semi-annual get-together, days filled with business updates, strategy sessions, good food and team building. Being a largely remote organization, these events are especially meaningful and rewarding. Our team has now grown to 12 but we are a tight-knit group and feeling more and more like a family as time goes by.

So this week, I’m vibin’ to the classic 1979 hit from Sister Sledge, We Are Family. Enjoy.

💭 Quote of the Week

“I’m putting all my money in taxes. They’re sure to go up.”

— Bob Hope

BONUS QUOTE

“Together is a beautiful place to be.“

— Melanie Allison

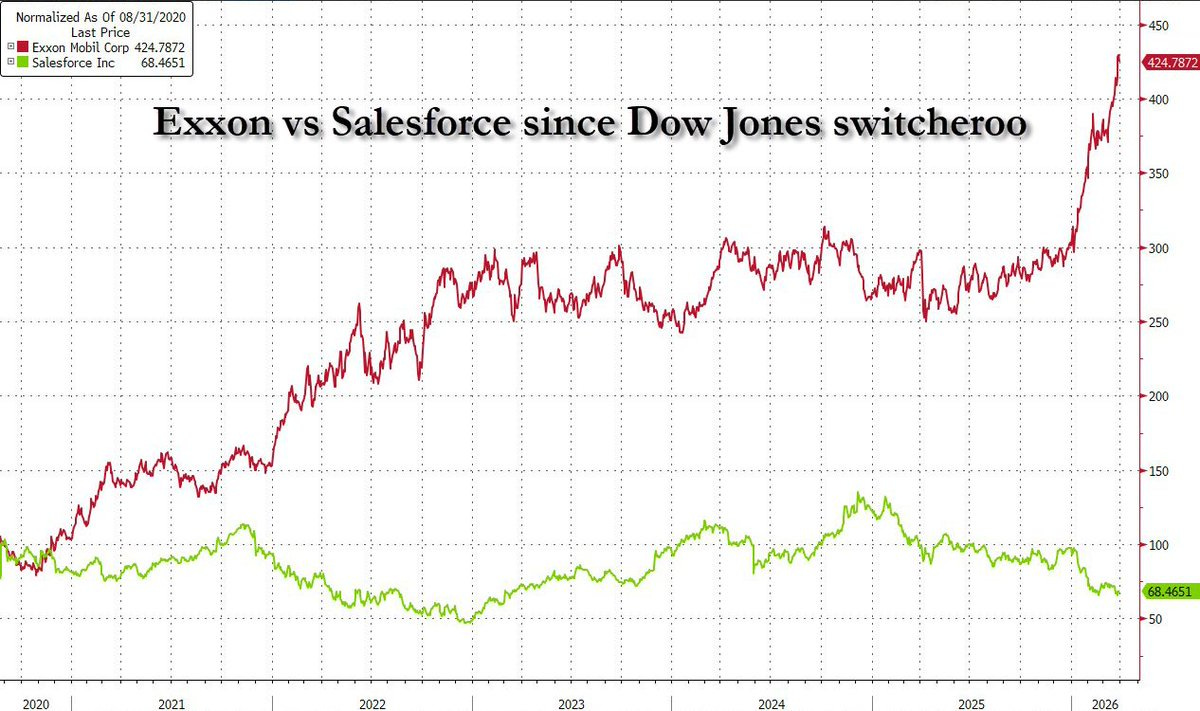

📈 Chart of the Week

The Dow’s Hall of Fame Problem

I found this week’s Chart to be not just interesting, but also borderline comical.

Since August 2020, Exxon Mobil, unceremoniously dumped from the Dow Jones Industrial Average after 92 consecutive years as a member, has returned roughly +271%. Salesforce, the company brought in to replace it, is down approximately -32%. That’s a gap of more than 300%, and it’s not a fluke. It’s a pattern.

The Dow committee removed Exxon at the worst possible moment: the COVID oil crash, with shares near $42, at peak pessimism about the future of fossil fuels. They added Salesforce at peak euphoria — a software darling trading at roughly 110x earnings. The committee was, in effect, selling the unloved and buying the beloved. Classic buy high, sell low.

And they’ve done it again. In November 2024, Intel, down 54% on the year and the Dow’s worst performer, was shown the door and replaced by Nvidia, which had just completed back-to-back years of gains of 240% and 170%. Returns since? Intel +40%, Nvidia +26%. The script is writing itself.

This isn’t just anecdotal. Arora, Capp, and Smith (2005) studied all Dow changes from 1929 through 2006 and found that in 32 of 50 cases, the deleted stock outperformed its replacement, with removed stocks averaging annualized returns of 15.9% versus 11.5% for additions over the following year.

Rob Arnott at Research Affiliates documented an even starker version of this in the S&P 500: additions entered at valuation premiums averaging over four times those of the stocks they replaced. He was so convinced by the data that he launched an ETF in 2024 specifically designed to buy index deletions and hold them for five years.

The structural reason is simple. The Dow uses purely subjective criteria: “reputation, sustained growth, and interest to a large number of investors.” Translation: companies get added when their cultural moment peaks. By the time a business is iconic enough for the Dow, its best growth is usually behind it. Walgreens, added June 2018, lost 63% in 2024 alone before being taken private. AIG, added in 2004, needed a $182 billion government bailout four years later. Microsoft and Intel, both added November 1, 1999, at the peak of the dot-com bubble, spent the better part of a decade underwater from their inclusion prices.

To be clear, not every deletion is a buy. Kodak, Sears, and Bethlehem Steel were all removed before going bankrupt. The signal is strongest when the removal reflects cyclical distress rather than secular decline: Exxon during COVID, GE during restructuring, Intel after missing the AI cycle. Those are the ones where the committee is extrapolating a bad trend at precisely the moment it could be about to reverse.

The Dow has a hall of fame problem: it inducts companies after they’ve already won. That’s great for plaques. It can be terrible for returns.

Source: StockCharts.com | ZeroHedge

🚙 Interesting Drive-By's 🚙

🤔 The Age of AI May Be the Best Argument Yet for the Liberal Arts

💡 70 Is the New 53 — And Voiceover Might Be the Real Fountain of Youth

👀 AI Is Already Showing Up in the Hard Data

💣 The Hole - Private credit is the fuse. The bomb is underneath the life insurance industry

😡 Why Does Everyone Hate AI? Luddites, Maslow’s Hierarchy, and a PR Crisis

👋🏼 Parting Thought

H/T to the Dragon Slayer…

If you have any cool articles or ideas that might be interesting for future Sunday Drive-by's, please send them along or tweet 'em (X ‘em?) at me.

Please note that the content in The Sunday Drive is intended for informational purposes only, and is in no way intended to be financial, legal, tax, marital, or even cooking advice. Consult your own professionals as needed. The views expressed in The Sunday Drive are mine alone, and are not necessarily the views of Investment Research Partners.

I hope you have a relaxing weekend and a great week ahead. See you next Sunday...

Your faithful financial provocateur,

-Mike

If you enjoy the Sunday Drive, I'd be honored if you'd share it with others.

If this was forwarded to you, please subscribe and join the other geniuses who are reading this newsletter.