The Sunday Drive - 03/29/2026 Edition [#208]

Musings and Meanderings of a Financial Provocateur

👋🏼 Hello friends! Let’s enjoy another Sunday Drive around the internet.

🎶 Vibin'

Markets are trying to process and price the uncertainties coming from the current conflict with Iran, in particular the knock-on effects of an extended closure of the Strait of Hormuz. What happens in that particular piece of geography over the coming weeks and months is a major pressure point for the global economy.

With that in mind, this week I’m vibin’ to the 1982 collaboration of Queen and David Bowie, Under Pressure, because that’s how investors, policy makers, and pretty much everyone are likely feeling these last few weeks.

💭 Quote of the Week

“You can make more friends in two months by becoming interested in other people than you can in two years by trying to get other people interested in you.“

— Dale Carnegie

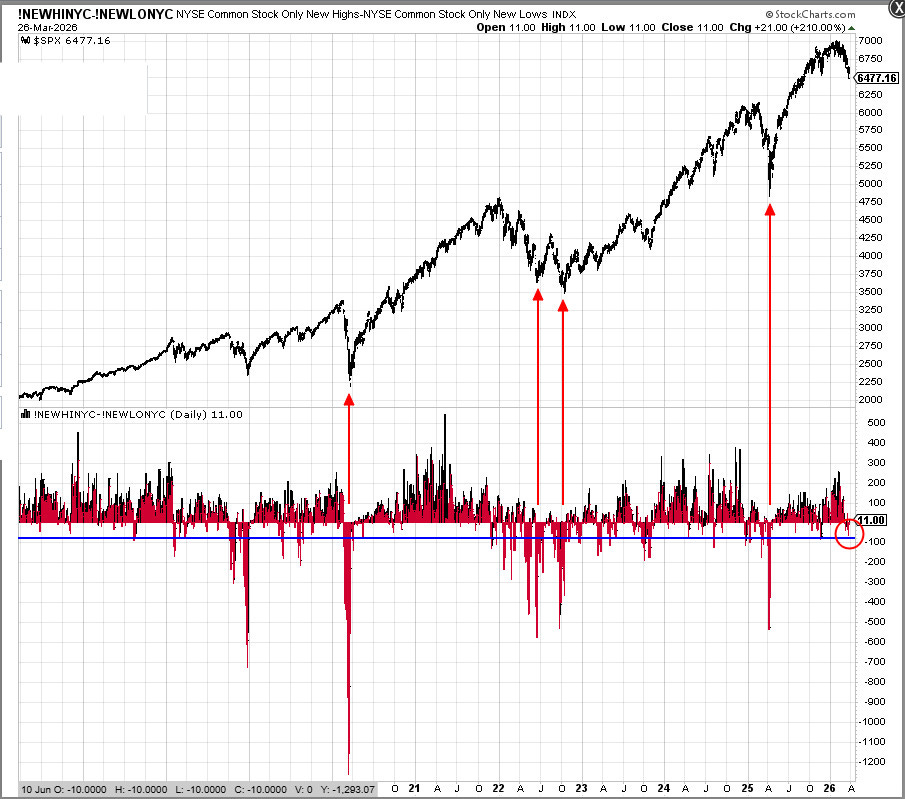

📈 Chart of the Week

Down But Not (Washed) Out

The S&P 500 closed last week at yet another year-to-date low, extending what is now its longest weekly losing streak since the 2022 bear market. If your social media feed and the financial headlines are any indication, you’d be forgiven for thinking the market is crashing.

But here’s the thing: the data isn’t confirming the panic, and to me, that’s actually the bearish part of the story this week’s Chart is telling us.

The Chart tracks NYSE New Highs minus New Lows, plotted beneath the S&P 500 going back 10 years. There’ve been four prior episodes where this breadth indicator crashed to deeply negative readings: the COVID collapse, the 2022 rate shock bear market, the 2023 growth scare, and the 2025 correction. Each of those red spikes downward corresponded with genuine, capitulation-level selling, the kind of indiscriminate, get-me-out-at-any-price washout that, historically, sets up powerful recoveries.

The S&P 500 is down 7% year-to-date.

Now look at the circled reading on the far right of the Chart. That’s where we are today: +11.

Not deeply negative. Not a washout. Not capitulation.

The distinction matters enormously. Feeling oversold and being oversold are two very different things. The market can absolutely bounce from here, and may well do so. But in my opinion, the breadth evidence is not yet consistent with a durable bottom. Prior lows that stuck were accompanied by breadth readings that looked far worse than what we’re seeing now. We haven’t seen that kind of broad-based, indiscriminate selling yet.

There’s more. Return dispersion across S&P 500 stocks has surged to more than 5 standard deviations above its long-term average, a level only seen during the Dot-Com crash, the Global Financial Crisis, and the COVID reopening. That kind of internal fragmentation is more characteristic of a market still searching for its footing than one that has found it.

Meanwhile, the Equal Weight S&P 500 and the Russell 2000 are barely clinging to their 200-day moving averages, while the S&P 500 and the Nasdaq have already slipped below theirs. The divergence between cap-weighted and equal-weighted indices is telling us something: this isn’t just a big-cap problem, but large caps are making it look worse than the average stock experience.

The macro backdrop isn’t helping. Volatility is elevated, though not extremely so, across all major asset classes simultaneously: equities, bonds, currencies, commodities. That kind of cross-asset volatility is unusual and typically signals that investors are repositioning broadly, not just rotating within equities.

The Takeaway: Sentiment is bearish. The headlines are scary. The losses are real. But the breadth data is telling us that the market hasn’t yet experienced the kind of panic-driven washout that typically marks a durable low. That doesn’t mean we can’t rally from here; markets do what they want. It means that investors looking for an “all clear” signal should probably wait for the data to confirm what the headlines are already screaming.

As I’ve said before, when you least expect it, expect it. The market has a way of delivering the most pain to the most people. Right now, it feels like many investors are positioned for a quick recovery. That alone gives me pause.

Patience, not panic. But not complacency either.

Source: YCharts | The Chart Report | Ned Davis Research

🚙 Interesting Drive-By's 🚙

💰 How America Quietly Got Rich

👀 The Liquidity Illusion is Cracking

🎯 AI’s Early Gift to Consumers

👋🏼 Parting Thought

Umm… Tiger, it might be time to let someone else do the driving from now on.

If you have any cool articles or ideas that might be interesting for future Sunday Drive-by's, please send them along or tweet 'em (X ‘em?) at me.

Please note that the content in The Sunday Drive is intended for informational purposes only, and is in no way intended to be financial, legal, tax, marital, or even cooking advice. Consult your own professionals as needed. The views expressed in The Sunday Drive are mine alone, and are not necessarily the views of Investment Research Partners.

I hope you have a relaxing weekend and a great week ahead. See you next Sunday...

Your faithful financial provocateur,

-Mike

If you enjoy the Sunday Drive, I'd be honored if you'd share it with others.

If this was forwarded to you, please subscribe and join the other geniuses who are reading this newsletter.