The Sunday Drive - 03/01/2026 Edition [#204]

Musings and Meanderings of a Financial Provocateur

👋🏼 Hello friends! Let’s enjoy another Sunday Drive around the internet.

🎶 Vibin'

Many of us “of a certain age” grew up in a world where there was a fairly well defined path. Get a good education. Find a good firm to be a part of, and contribute to. Build a career.

But these days, there seems to be much to worry about in terms of what many professional paths might look like in the future, much that doesn’t seem logical or sensible or predictable.

So this week, I’m vibin’ to Supertramp’s classic, The Logical Song.

💭 Quote of the Week

“Faith is to hope for things which are not seen but which are true. Therefore, please, […] my dear friends, first doubt your doubts before you doubt your faith.“

— Dieter F. Uchtdorf

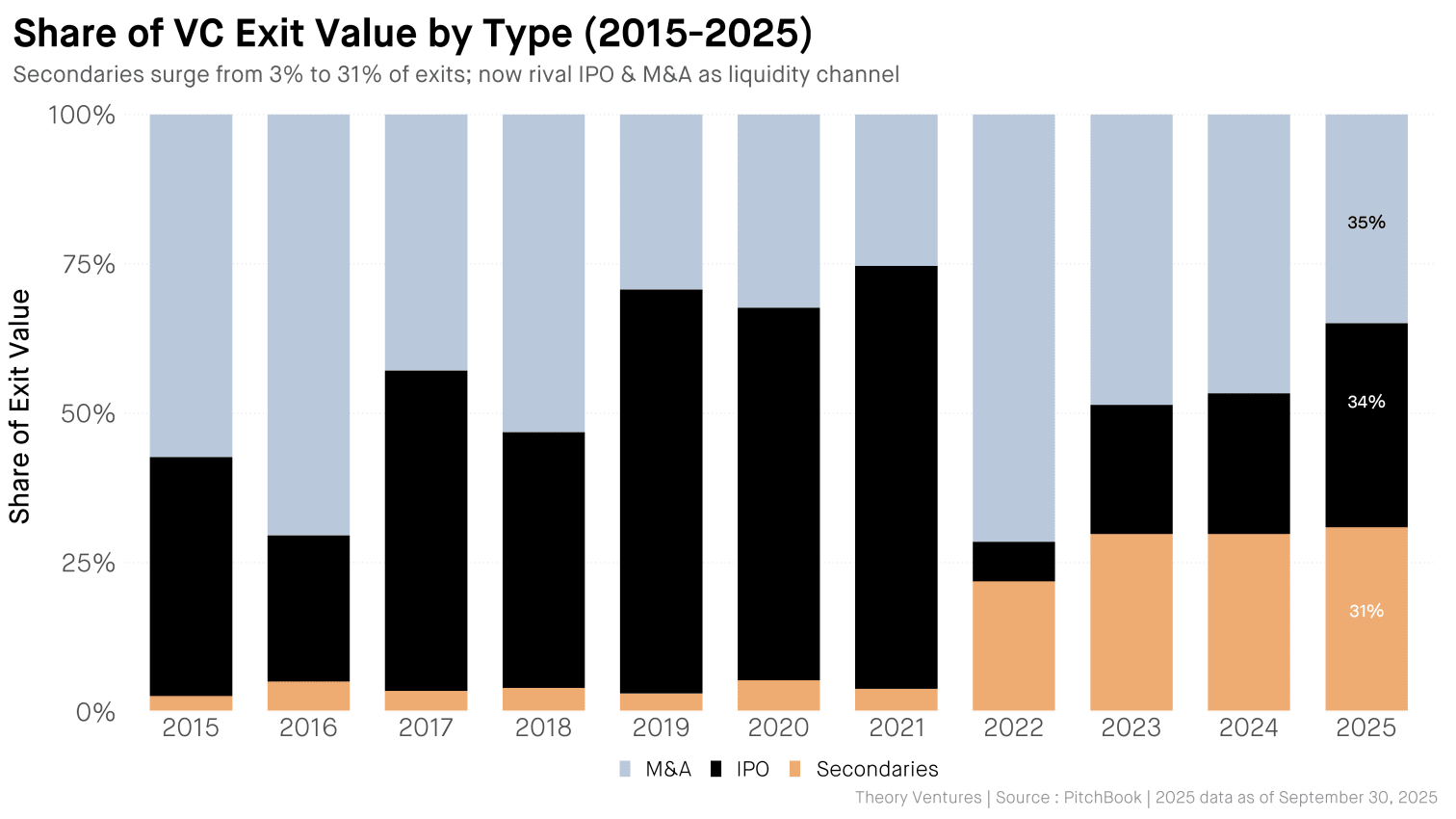

📈 Chart of the Week

On Second Thought…

For decades, venture capital operated on a simple exit playbook: build, scale, and eventually distribute gains through an IPO or strategic sale. This week’s Chart shows that exits have become “a third, a third, a surprising third”. The playbook seems to have been quietly rewritten. Secondary transactions, just 3% of exits a decade ago, now rival IPOs and M&A as a core liquidity channel.

At its core, a secondary transaction is simply the transfer of existing ownership. No new capital reaches the company. Instead, liquidity flows to founders, employees, early investors, or limited partners (LPs) who want to rebalance risk or return capital. What’s changed is not the mechanism, but the motivation and scale.

One innovation engine has been the General Partner (GP)-led continuation fund. Rather than selling crown-jewel assets into a weak IPO or M&A market, managers now roll them into new vehicles, offering existing LPs a choice: cash out or stay invested. This vehicle appears to have solved a structural mismatch: venture funds have finite lives, but great companies compound over decades. Continuation funds effectively refinance duration.

A second form, LP-led secondaries, have evolved from distress sales into portfolio management tools. Large allocators now actively shape vintage exposure, geography, and sector weightings through secondary sales.

Direct secondaries add a third layer, enabling employee liquidity programs that double as talent retention tools, a subtle but powerful shift in how private companies compete for human capital.

Macro forces accelerated the shift. When the IPO window effectively closed in 2022 and distributions evaporated, secondaries filled the void. Liquidity didn’t disappear; it rerouted.

Today’s estimated $130–150 billion annual secondary market across private assets reflects institutional acceptance, tighter pricing spreads, and specialized buyers ranging from dedicated secondary funds to sovereign wealth capital. (Source: Pitchbook).

The implications extend beyond venture capital. A robust secondary market reduces liquidity risk, lowers the cost of capital, and may ultimately support higher private-market allocations in institutional portfolios. In effect, secondaries transform venture capital from a blind-pool, long-duration bet into a more actively managed asset class.

Speculatively, we may be watching the emergence of what might think of as a true private-market yield curve, where duration, liquidity, and pricing can be actively traded rather than passively endured. If so, the “surprising third” isn’t just a new exit path. It’s a structural evolution in how capital compounds outside public markets.

On second thought, the real story isn’t that secondaries grew. It’s that venture capital may have finally built a liquidity mechanism sophisticated enough to match the scale of the ecosystem it created.

🚙 Interesting Drive-By's 🚙

💯 The Week AI Stopped Asking Permission

🤔 Latest Data on State Income Tax Rates Reveals a Widening Divide in America

🎯 The End of Work? Not Yet - Maybe Not Ever

💡 What I’m Telling My Kids About AI

📈 The Number Is Going Up: AI Speculation, Market Concentration, and the Upward Vacuum of Value

👋🏼 Parting Thought

The AI angst that many folks are wrestling with these days…

If you have any cool articles or ideas that might be interesting for future Sunday Drive-by's, please send them along or tweet 'em (X ‘em?) at me.

Please note that the content in The Sunday Drive is intended for informational purposes only, and is in no way intended to be financial, legal, tax, marital, or even cooking advice. Consult your own professionals as needed. The views expressed in The Sunday Drive are mine alone, and are not necessarily the views of Investment Research Partners.

I hope you have a relaxing weekend and a great week ahead. See you next Sunday...

Your faithful financial provocateur,

-Mike

If you enjoy the Sunday Drive, I'd be honored if you'd share it with others.

If this was forwarded to you, please subscribe and join the other geniuses who are reading this newsletter.