The Sunday Drive - 10/26/2025 Edition [#186]

Musings and Meanderings of a Financial Provocateur

👋🏼 Hello friends! Today is my birthday, along with two longtime friends and Eaton Vance colleagues - a trio of Scorpios. Please celebrate with us by enjoying a leisurely Sunday Drive around the internet.

🎶 Vibin'

This week, I’m vibin’ to a power ballad about the hope and optimism surrounding the end of the Cold War. The song ultimately became an anthem for peace and reconciliation, symbolizing not only the fall of the Berlin Wall and the collapse of the Soviet Union but also the universal yearning for freedom and unity among people everywhere. I think the world could use a bit more of that these days.

I’ve long been a fan of The Scorpions, for obvious reasons. 🙂 I hope you enjoy their 1989 hit, Wind of Change.

💭 Quote of the Week

“October: This is one of the peculiarly dangerous months to speculate in stocks. The others are July, January, September, April, November, May, March, June, December, August, and February.’

— Mark Twain

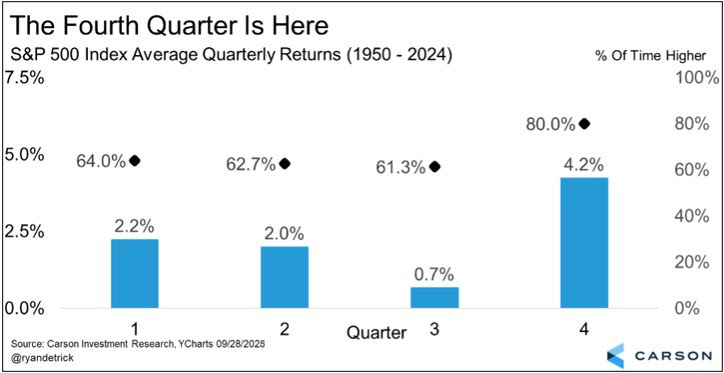

📈 Chart of the Week

Seasonality…. Am I right?

The Chart of the Week shows that 3rd quarter performance for the S&P 500 is historically by far the weakest quarter of the year. Q4 performance by contrast is historically the strongest period, and by a significant margin.

After a solid year-to-date showing in the first half of the year, with the S&P 500 up 6.2%, most experienced investors and prognosticators had what many could reasonably consider quite modest expectations for Q3, including me. After all, that would be consistent with the historical pattern—poor performance with lots or volatility.

Well…

As well known investment newsletter publisher, Jared Dillian once wrote, “The market always does what makes you feel the most stupid.”

Aaaaand that’s exactly what the equity market did in Q3—at least to me. The S&P 500 ended the period up 8.12%, well above the first half performance, and it did so with very low volatility. The VIX, which measures market volatility, with the exception of one day, was below its long term average level of 20 every day in the quarter. Through the end of Q3, the S&P 500 stood at +14.8% year-to-date.

How might we expect the equity market to perform in Q4?

After the very strong performance by the S&P 500 in 2023 and 2024, up 26.3% and 25.0%, respectively, and with the strong year-to-date performance thus far in 2025, one might be forgiven for being a bit cautious as we approach year-end.

However, if the historical pattern holds in Q4, then the market would be on a pace to have yet another +20% year.

My forecast?

My highest conviction forecast is that the market will find a way, yet again, to make me feel stupid.

Source: YCharts.

🚙 Interesting Drive-By's 🚙

💰 JPMorganChase Launches $1.5 Trillion Security and Resiliency Initiative

📈 Famous Strawmen: The Scarecrow & the Best 10 Days Rule

🎯 AI is the Market, and the Market is the Government

👋🏼 Parting Thought

If you have any cool articles or ideas that might be interesting for future Sunday Drive-by's, please send them along or tweet 'em (X ‘em?) at me.

Please note that the content in The Sunday Drive is intended for informational purposes only, and is in no way intended to be financial, legal, tax, marital, or even cooking advice. Consult your own professionals as needed. The views expressed in The Sunday Drive are mine alone, and are not necessarily the views of Investment Research Partners.

I hope you have a relaxing weekend and a great week ahead. See you next Sunday...

Your faithful financial provocateur,

-Mike

If you enjoy the Sunday Drive, I'd be honored if you'd share it with others.

If this was forwarded to you, please subscribe and join the other geniuses who are reading this newsletter.

Happy birthday, Mike!

Speaking of Winds of Change... here's a pod by Patrick Radden Keefe (New Yorker) investigating whether Winds of Change was written by the CIA.

Have a great day!